150+ minds across 4 countries. Join a culture of innovation, ownership & growth.

Rewire for AI

From machine learning to deep learning, from classification tools to overall process automation – our AI engineers will help you retool your existing system or enhance your company results.

Ship faster, scale smarter, built for product companies and SaaS teams

Our Latest Work

We strive hard to deliver result-driven digital solutions across the globe. Check out our case studies to get a glimpse of how we ideate, innovate, and create unconventional digital solutions according to the requirements of our clients.

Discover diverse and passionate insights from our tech enthusiasts. We collaborate across various sectors to streamline operations and drive innovation. Explore our rapidly growing collection of articles to see why we’re at the forefront of IT solutions.

The decision to move from Magento to Shopify is one of the most significant replatforming choices an ecommerce business can make. Magento is powerful, but its power comes with...

Accuracy gap is real: Traditional CPG forecasting carries a 25-40% MAPE error rate. AI-powered models bring that down to 8-15%, according to McKinsey research....

Real stories from global leaders who trusted us with their ideas.

Partnering with APPWRK helped us build a compliant and scalable healthcare platform, accelerating our time-to-market by 35%. Their team consistently delivered outstanding work.

Beesers

Digital Healthcare Client

Collaborating with APPWRK, Sportskeeda modernized its platform into a real-time sports engagement ecosystem, enabling seamless content delivery, scalable fan interactions, and high-velocity performance.

Sportskeeda

Sports & Entertainment Partner

Working with APPWRK was effortless. They captured our vision, maintained full compliance, and delivered a digital experience that built trust and elevated how customers interact with our fintech brand.

PayPenny

Fintech Partner

Working with APPWRK gave us confidence in adopting AI responsibly. Their team built a safe, intelligent bot that transformed how we engage with leads and helped us achieve measurable revenue growth.

IFB

AI Transformation Partner

Leveraging APPWRK’s digital expertise, Nemesis launched a scalable, compliant, and safe super app that connects content delivery, real-time communication, and logistics management within a single platform.

Address management is a core identity pillar that directly impacts bank onboarding speed, compliance accuracy, and fraud prevention. As global banks scale both corporate and retail banking, modernising address processes becomes essential for a smooth customer onboarding experience.

Banks must shift from manual, form-heavy address capture to automated, API-first, normalised address workflows. This transformation improves the digital onboarding experience, supports mobile-first design, and strengthens both business-to-business (B2B) onboarding and business-to-consumer (B2C) onboarding journeys.

RegTech-driven verification, PKYC, and intelligent data orchestration enhance KYC due diligence by validating addresses against sanctions screening, politically exposed persons (PEPs), watchlists, and corporate registries. These steps reduce onboarding friction while maintaining compliance standards across global banks and corporate clients.

Effective governance ensures that data remains reliable throughout the end-to-end onboarding experience, enabling a seamless multichannel experience and reducing onboarding operating costs. With more accurate address intelligence, banks can accelerate time-to-revenue, eliminate redundant manual reviews, and strengthen long-term customer trust in digital onboarding in financial services.

Introduction – Why Address Management Determines Digital Onboarding Success

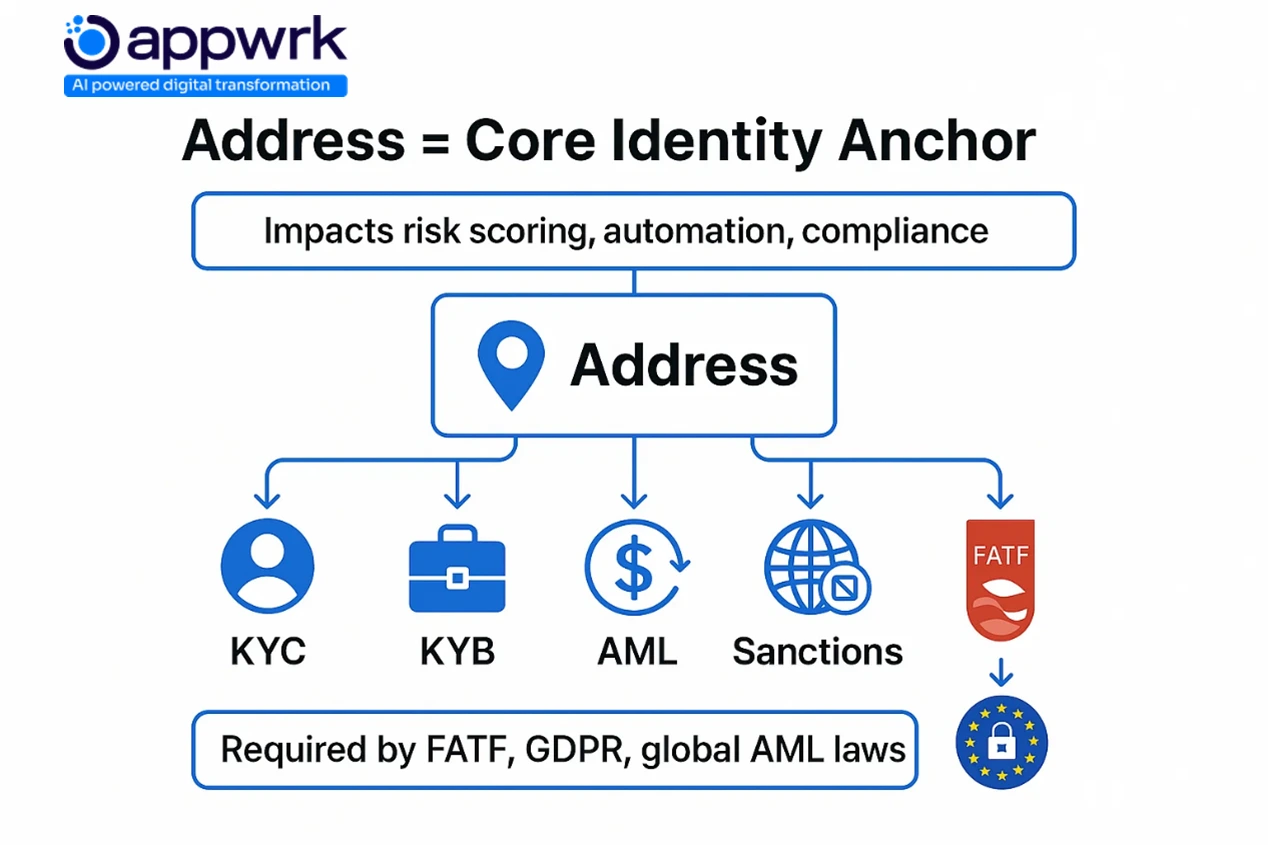

Address data is foundational to KYC, KYB, AML, and fraud prevention. Financial institutions rely on accurate verification to confirm identity, meet global compliance standards, and protect against financial crime. For global banks operating across corporate and retail banking, reliable address intelligence is essential to delivering a smooth customer onboarding experience.

Yet many institutions still face fragmented data sources, inconsistent global address formats, and heavy manual validation. These gaps slow the digital onboarding experience, increase onboarding drop-offs, and raise compliance risks, especially during KYC due diligence for both business-to-business (B2B) onboarding and business-to-consumer (B2C) onboarding.

Modern address management powered by real-time validation, smart APIs, and RegTech automation significantly improves the end-to-end onboarding experience. It also lowers onboarding operating costs, accelerates time-to-revenue, and enhances risk scoring through better checks against sanctions screening, politically exposed persons (PEPs), watchlists, and corporate registries.

With digital onboarding in financial services becoming increasingly mobile-led, workflows built for mobile-first design, automation, and speed are no longer optional. They are critical to delivering a seamless multichannel experience, reducing friction for corporate clients, and future-proofing onboarding operations across all channels of an omnichannel experience.

The Role of Address Data in Modern Digital Onboarding

Address data plays a pivotal role in digital onboarding in financial services because it acts as a primary identity anchor across KYC, KYB, AML, sanctions checks, and ongoing monitoring. For global banks and institutions operating in both corporate and retail banking, the ability to verify addresses quickly and accurately is essential for fraud prevention, regulatory compliance, and a smooth customer onboarding experience.

Global regulations such as FATF, GDPR, and AML directives require precise address handling and transparent ownership traceability. Any gaps during account opening delay the end-to-end onboarding experience, increase compliance risk, and raise onboarding operating costs, especially across business-to-business (B2B) onboarding and business-to-consumer (B2C) onboarding workflows.

Accurate address data strengthens KYC due diligence, supports automated processes, enables reliable checks against sanctions screening, politically exposed persons (PEPs), watchlists, and corporate registries, and improves risk decisioning. It also reduces friction for corporate clients and consumers, enhancing the overall digital onboarding experience, especially in mobile-first design environments and omnichannel experience models.

Clear, standardised, and validated address intelligence improves user experience, accelerates time-to-revenue, and ensures onboarding journeys deliver a seamless multichannel experience.

Impact of Clean Address Data on Banking Onboarding

Clean, structured address data is essential for delivering a frictionless customer onboarding experience across corporate and retail banking. It directly affects regulatory compliance, fraud prevention, operational efficiency, and how quickly banks move customers from registration to activation, improving time-to-revenue and lowering onboarding operating costs. For global banks, ensuring accurate address data strengthens digital onboarding in financial services and reduces risk across both business-to-business (B2B) onboarding and business-to-consumer (B2C) onboarding.

Impact Area

With Clean Address Data

With Dirty Address Data

Regulatory Compliance (KYC/AML)

Enables fast, audit-ready identity verification and PoA validation, improving KYC due diligence, sanctions screening, PEPs, and watchlist checks.

Leads to delays, failed audits, and regulatory penalties due to unverifiable information.

Supports real-time anomaly detection, reducing synthetic ID and identity fraud risk.

Increases exposure to fraud, money laundering, and compliance violations.

Customer Experience

Speeds up digital onboarding experience, minimises form errors, and reduces re-verification cycles, strengthening seamless multichannel experience.

Causes abandonment, frustration, and poorer satisfaction across mobile and web channels.

Operational Efficiency & Cost

Enables automation (smart autofill, instant validation), reducing manual work and internal processing costs.

Triggers rework, manual review queues, and inefficiencies that raise onboarding costs.

Communication & Service Delivery

Ensures accurate delivery of Cards, bank mail, regulatory notices, and digital communications.

Causes include lost Cards, missed notifications, and declining trust, negatively impacting NPS.

Risk Management

Supports accurate location-based risk scoring and better decisions across lending, underwriting, and compliance.

Weakens credit insights and raises risk across decisioning workflows.

Clean address workflows are no longer optional; they’re mission-critical for scalable digital onboarding in financial services, especially as corporate clients and retail users demand faster, safer, mobile-first experiences.

Common Address-Related Friction Points in Banking Onboarding

Customer onboarding processes in the banking industry often stall due to fragmented address workflows and outdated infrastructure. These gaps reduce efficiency across digital onboarding infinancial services, increase compliance risks, and disrupt both business-to-business (B2B) onboarding and business-to-consumer (B2C) onboarding journeys. Below are the most common friction points affecting the customer onboarding experience and the end-to-end onboarding experience.

Manual Entry

Many legacy systems still depend on manual address entry, creating errors, inconsistencies, and formatting issues. These inaccuracies slow KYC due diligence, trigger additional checks against sanctions screening, politically exposed persons (PEPs), and watchlists, and often lead to failed onboarding attempts, hurting the overall digital onboarding experience.

Data Inconsistency Across Systems

Disconnected CRM systems, document repositories, and compliance platforms create repetitive address validation. This leads to mismatched customer data, delays straight-through-processing, increases onboarding operating costs, and weakens onboarding accuracy for corporate clients and retail users.

Legacy Core Banking Constraints

Traditional corporate and retail banking platforms lack API-enabled address validation, blocking automation and real-time updates. Without modern integrations, banks struggle to support mobile-first design, maintain address consistency, or deliver a seamless multichannel experience across web, branch, and mobile channels.

Global Format Variation

Banks operating across borders face significant challenges due to non-standard global address formats. From Japanese multi-line structures to European codes, inconsistent rules make cross-border onboarding complex. Without standardisation, global banks risk compliance gaps, operational delays, and misclassification during digital onboarding experience checks.

Customer Drop-Offs Due to Repeated Verification

Mobile and web onboarding journeys often force users to re-enter the same address due to formatting mismatches or validation failures. As a report from One World Identity found, where friction is met in the digital onboarding process requiring presentation of identity documentation (scanning and emailing copies, mailing paper copies, or having to provide original copies in person), 25% of applicants will abandon the process and go elsewhere.

7 Essential Methods to Improve Address Management

As digital transformation accelerates in banking, address accuracy has become a critical foundation for secure, seamless, and compliant onboarding. These seven methods help banks, fintechs, and financial institutions enhance address workflows, reduce friction, and improve the customer onboarding experience across both business-to-business (B2B) onboarding and business-to-consumer (B2C) onboarding.

1. Improve CX With Auto-Fill & Smart Validation

Auto-fill, powered by verified sources and an intelligent validation API, delivers standardised, typo-free entries, reducing errors and form abandonment. This directly improves the digital onboarding experience, especially in mobile-first design journeys, and enhances the overall end-to-end onboarding experience.

2. Simplify Address Capture & Mobile Readability

Smartphone-optimised forms with responsive layouts and predictive search elevate the onboarding flow for both retail users and corporate clients. Clean, mobile-ready UI reduces input mistakes, lowers onboarding operating costs, and strengthens the omnichannel experience.

3. Strengthen Cybersecurity & Fraud Detection Using Address Signals

Cross-referencing address inputs with device fingerprints, digital footprints, and behavioural signals helps detect synthetic identities and high-risk patterns. This supports stronger KYC due diligence, complements checks against sanctions screening, politically exposed persons (PEPs), and watchlists, and enhances fraud prevention during digital onboarding in financial services.

4. Provide Assisted Resolution for Address Mismatches

Automated suggestions, partial-match prompts, and real-time support reduce onboarding drop-offs caused by validation gaps. Address anomaly detection ensures smoother onboarding and improves the seamless multichannel experience without adding friction for the final consumer.

5. Use PKYC for Ongoing Address Monitoring

Perpetual KYC (PKYC) enables continuous monitoring of address changes and ownership updates. This supports enhanced due diligence in corporate and retail banking, reduces compliance risk, and ensures address accuracy throughout the customer lifecycle, helping global banks manage risk and accelerate time-to-revenue.

6. Centralise Address Data Across CRM, Core Banking & CLM

Creating a unified customer information hub across CRM, core banking, and lifecycle management platforms helps banks eliminate manual processes and maintain consistent records. This improves straight-through-processing, reduces duplication in KYC due diligence, and strengthens confidence for both global banks and corporate clients.

7. Enable Global Address Orchestration via APIs

API-first orchestration standardises and validates addresses across borders, enabling consistency across onboarding, trade finance, payments, and cash management workflows. Platforms like Trulioo and Hummingbird help financial institutions maintain compliance with corporate registries, support a digital onboarding experience at scale, and ensure accuracy across diverse international formats.

How Address Management Enhances STP, KYC APIs, and Entity Verification

Straight-through-processing (STP), KYC APIs, and entity verification all depend on clean, standardised, and continuously monitored address data. When address inputs are validated in real time and normalised across systems, onboarding becomes faster, more accurate, and easier to scale, improving the overall customer onboarding experience across both business-to-business (B2B) onboarding and business-to-consumer (B2C) onboarding. For global banks, strong address intelligence supports automation and strengthens digital onboarding in financial services.

1. Supporting Straight-Through-Processing (STP)

STP requires structured, machine-readable address data that can move through onboarding workflows without manual review. Clean address data enables:

Automated routing of applications across onboarding and compliance paths

Reduction of verification exceptions caused by mismatches

For corporate clients, especially in trade finance, payments, and cash management, effective STP improves processing timelines and enhances the end-to-end onboarding experience while reducing drop-offs across omnichannel experience journeys.

KYC APIs rely on validated address inputs to perform high-assurance checks across global datasets. Normalised address data improves API performance by ensuring:

Higher match rates with government sources and third-party databases

More reliable ingestion for KYC due diligence and AML checks

Consistent cross-channel verification outcomes

Aligned schemas support auto-fill capabilities, reduce repeated inputs, and minimise false positives/negatives in compliance assessments, all strengthening the digital onboarding experience.

3. Strengthening Entity Verification for Corporate Customers

For corporate onboarding, accurate address data helps institutions verify legitimacy, ownership, and operational presence. Clean, validated address records enable:

Cross-checking against corporate registries for entity-level verification

Identification of discrepancies in ownership or control

Detection of synthetic identity risks tied to inconsistent locations

For complex corporate networks in corporate and retail banking, this enhances downstream compliance checks, including sanctions screening, PEPs, and watchlists.

4. Enabling Integrated Risk Evaluation Across Systems

Address alignment across CRM, document management, and onboarding systems ensures:

Cohesive risk assessment logic across teams

Accurate aggregation of location-linked risk indicators

Cross-system automation for ongoing monitoring and lifecycle management

This reduces duplicated compliance reviews, accelerates time-to-revenue, and improves the seamless multichannel experience for both retail and corporate clients.

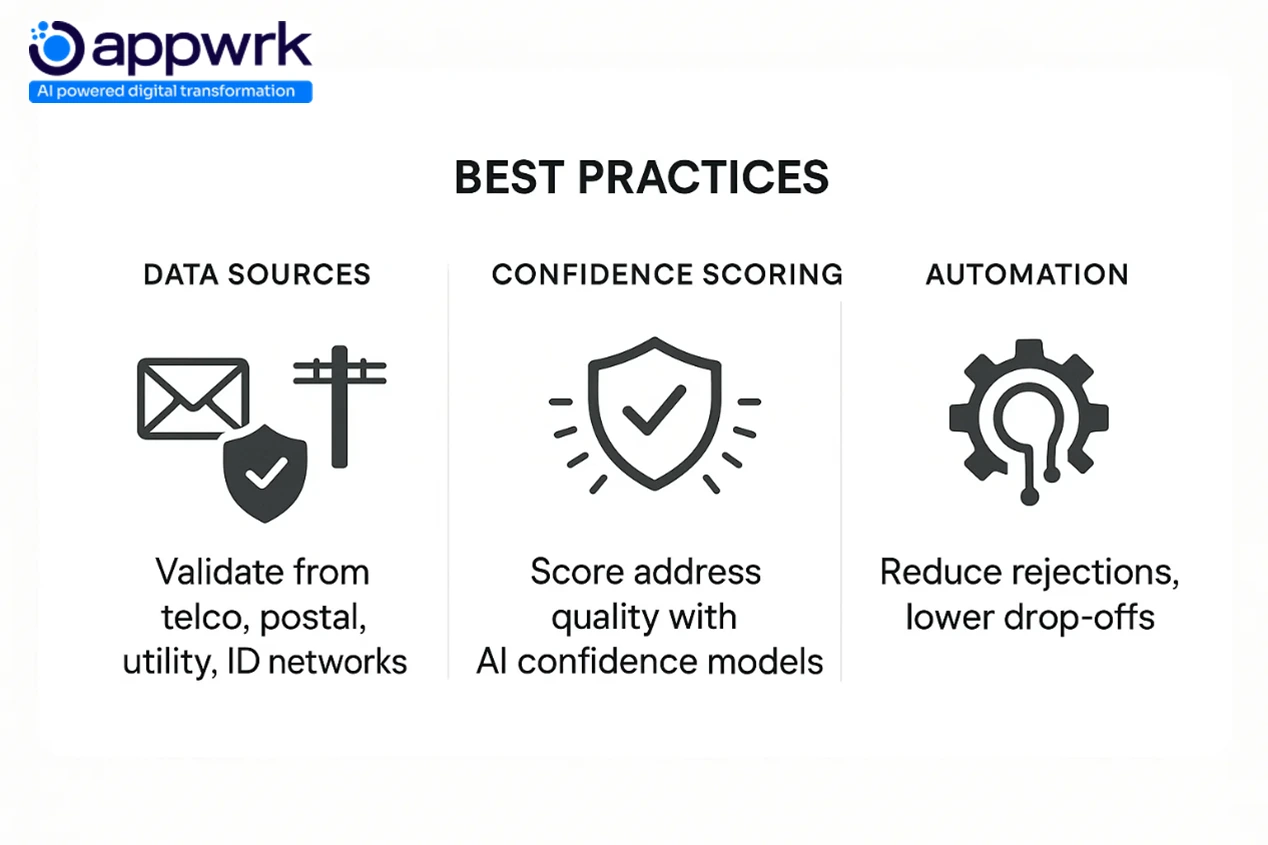

Best Practices for Enterprise-Grade Address Verification

To ensure customer onboarding banking meets global regulatory standards, banks must adopt enterprise-grade address verification frameworks that go beyond basic checks. Leading global banks and financial institutions use the following best practices to strengthen compliance, reduce friction, and enhance the customer onboarding experience across both corporate and retail banking.

Multi-Source Validation

Pulling address data from postal, telco, utilities, and government sources improves overall identity integrity. This strengthens KYC due diligence, enhances checks against sanctions screening, politically exposed persons (PEPs), and watchlists, and reduces synthetic ID risk for both business-to-business (B2B) onboarding and business-to-consumer (B2C) onboarding.

Address Confidence Scoring

Machine learning models and behavioural analytics help institutions score address inputs for trustworthiness. This improves risk decisioning, reduces false positives, and creates a smoother digital onboarding experience across all channels, including mobile, branch, and web.

Reducing Reject Rates and Friction

Advanced tools such as eSignature, ID scanning, and liveness detection reduce manual reviews. The result is faster onboarding, less user frustration, and improved end-to-end onboarding experience, ultimately lowering onboarding operating costs and accelerating time-to-revenue.

Integration With Document & Workflow Systems

Embedding address verification into document management systems (e.g., SharePoint, KanBo) streamlines account opening and reduces manual touchpoints. This supports a seamless multichannel experience, especially for mobile-first design environments and high-volume digital onboarding in financial services.

RegTech Integrations for Address Screening & Ongoing Monitoring

Modern onboarding requires more than static address checks. RegTech integrations enable banks to automate address screening, adapt to evolving compliance requirements, and improve long-term monitoring across corporate clients and retail users.

Real-time tools like Trulioo, Onfido, and Hummingbird validate addresses instantly against global data networks. These solutions flag anomalies, track ownership structures, and run sanctions screening, PEP checks, and watchlists in the background, supporting PKYC and AML controls.

Integration into workflow systems like KanBo and SharePoint

Audit-ready compliance trails for regulators

These integrations not only improve compliance but also support digital onboarding in financial services at scale without compromising customer satisfaction or efficiency.

Address Management in Corporate vs Retail Onboarding

Address data plays different roles in corporate banking compared to retail. Understanding these differences ensures smoother onboarding and stronger compliance for both segments across global banks.

Complex ownership structures validated against corporate registries

These checks support trade finance, cash management, and document-heavy processes, ensuring higher accuracy during business-to-business (B2B) onboarding.

Retail Users

Retail onboarding emphasises speed, automation, and user-friendly flows, including:

Biometric verification

eSignature and ID capture

Mobile-first design interfaces

Instant address matching for faster business-to-consumer (B2C) onboarding

Retail customers expect a frictionless, self-service experience across digital channels.

Shared Requirement

Both corporate and retail onboarding depend on scalable, standardised address orchestration. Consistent, validated address data ensures a seamless multichannel experience, reduces regulatory exposure, and enhances the overall customer onboarding experience.

Unified address workflows significantly elevate customer experience and strengthen compliance across all channels.

Modern client onboarding faces rising complexity from inconsistent address data and global regulatory pressures. These challenges directly affect the customer onboarding experience, digital onboarding experience, and overall time-to-revenue for global banks. Here are key issues and how financial institutions can solve them:

Data Quality Gaps

Unverified or outdated address entries reduce identity verification success and increase failure rates during KYC due diligence and sanctions screening. Mitigation: Use digital tools and real-time data sources to auto-correct and validate entries across corporate and retail banking systems to support a seamless omnichannel experience.

Regulatory Fragmentation

Cross-border operations introduce varying AML rules and address formats, creating onboarding friction for both business-to-business (B2B) onboarding and business-to-consumer (B2C) onboarding. Mitigation: Integrate multi-jurisdiction validation APIs and centralised policy rules to maintain consistent digital onboarding in financial services.

High Verification Latency

Manual reviews cause onboarding delays, raising operational costs and increasing drop-offs during the end-to-end onboarding experience. Mitigation: Accelerate verification using automation, biometrics, eSignature, and risk-based smart routing.

Synthetic Address Fraud

Fraudsters increasingly use synthetic addresses to bypass identity checks and exploit compliance gaps. Mitigation: Use digital footprint matching, liveness detection, and fraud detection tools that cross-reference device signals and behaviour.

Address Governance Framework for Large Banks

For global banks, weak address governance amplifies onboarding delays and creates data inconsistencies across risk, compliance, and operational teams. A strong governance model ensures that every customer onboarding process operates on clean, standardised, compliant data.

Key pillars of address governance include:

Enterprise-Wide Ownership

Assign data ownership across compliance, operations, and risk teams to eliminate silos in customer data and strengthen corporate clients’ onboarding integrity.

Schema Standards & Validation Rules

Define global templates to normalise address capture across web portals, CRM systems, and document tools like SharePoint or KanBo, improving digital onboarding experience consistency.

Continuous Monitoring

Enable real-time anomaly alerts, dashboards, and automated notifications to maintain address accuracy and support ongoing AML compliance. This drives faster approvals across Cards, origination, and commercial banking workflows.

Strong governance also reduces onboarding operating costs, improves SLAs, and enhances the overall seamless multichannel experience.

How Appwrk Helps Modernise Address Management for Global Banks

Appwrk provides an API-first address management layer designed for global banks aiming to modernise onboarding across corporate and retail banking.

Key capabilities include:

Secure integrations with global data providers for real-time verification, sanctions screening, PEP checks, and watchlist matching

Automation for document matching, ownership validation, and identity verification to enhance KYC due diligence

Seamless alignment with core banking, CRM, and document management systems to strengthen the end-to-end onboarding experience.

Support for cross-border onboarding, including Cards, commercial banking, and trade finance, enabling frictionless digital onboarding in financial services

With Appwrk, banks cut onboarding time, improve compliance accuracy, and upgrade the customer onboarding experience, all while reducing overall operational overhead.

Real-world Impact by Appwrk

Appwrk helped Unilever optimize data visibility through a custom dashboard system integrated with secure access controls. The solution enhanced internal decision-making and compliance tracking, offering a model for banks aiming to modernize their customer onboarding processes with clean address data and real-time analytics.

Founder’s Guide — Building a Future-Ready Address Management Strategy

Founders building digital-first financial platforms need scalable address workflows to support evolving regulations, global reach, and modern customer expectations.

Decision Framework

Evaluate whether to build or buy based on internal resources, regulatory requirements, and the need for integrated experiences across portals, CRM, and document systems.

Migration Roadmap

Retire legacy address workflows and adopt mobile-enabled, API-first, compliance-ready infrastructure to support a high-quality mobile-first design and seamless multichannel experience.

KPIs to Track

Address verification success rate

Drop-offs in account opening

Average time-to-fulfilment

NPS and post-onboarding customer satisfaction

With the right foundation, address workflows become a competitive advantage, reducing time-to-revenue, improving compliance, and elevating the entire digital onboarding experience.

FAQs

What is the onboarding process for banks? The onboarding process includes collecting customer information, validating identity and address, performing KYC due diligence, and completing AML checks such as sanctions screening, PEP checks, and watchlists before activation. These steps shape the overall customer onboarding experience and help reduce risk for global banks.

What are the 7 steps of client onboarding? Most banks follow seven stages: client registration, data collection, identity verification, document review, compliance checks, account setup, and final client activation. These steps ensure a smooth end-to-end onboarding experience across both business-to-business (B2B) onboarding and business-to-consumer (B2C) onboarding.

What are the 7 P’s of banking? Product, Price, Place, Promotion, People, Process, and Physical Evidence form the core of the banking marketing mix and influence both corporate and retail banking engagements.

What are the 5 stages of KYC? Customer identification, risk assessment, document collection, enhanced due diligence (when required), and continuous monitoring. These steps support safer digital onboarding in financial services and reduce onboarding operating costs.

Is there anything banks could do to improve the onboarding experience? Yes, banks can improve automation, streamline data entry, use mobile-first biometric verification, and centralise data to deliver a faster, more compliant digital onboarding experience with a seamless multichannel experience.

What’s the difference between corporate and retail onboarding? Corporate onboarding requires deep verification of corporate registries, ownership structures, and trade finance needs, while retail onboarding prioritises speed, simplicity, and mobile-first design. Both rely on accurate address management to reduce latency and improve time-to-revenue.

How can Appwrk support address verification for onboarding? Appwrk provides real-time validation, AI-based orchestration, and seamless integration with CRM and core systems, helping global banks deliver faster, safer onboarding across corporate clients and retail users while enhancing compliance and overall customer onboarding experience.

Gourav Khanna is the Co-founder and CEO of APPWRK, leading the company’s vision to deliver AI-first, scalable digital solutions for enterprises and high-growth startups. With over 16 years of leadership in technology, he is known for driving digital transformation strategies that connect business ambition with outcome-focused execution across healthcare, retail, logistics, and enterprise operations.

Recognized as a strategic industry voice, Gourav brings deep expertise in product strategy, AI adoption, and platform engineering. Through his insights, he helps decision-makers prioritize market traction, operational efficiency, and long-term ROI while building resilient, user-centric digital systems.

Subscribe to APPWRK Blogs, We'll Do the Rest!

Get Blogs on UI/UX, Mobile Apps, Online Marketing, and Web development technology.

Unlock worthy and priceless suggestions from the masters of mobile and web app development