150+ minds across 4 countries. Join a culture of innovation, ownership & growth.

Rewire for AI

From machine learning to deep learning, from classification tools to overall process automation – our AI engineers will help you retool your existing system or enhance your company results.

Ship faster, scale smarter, built for product companies and SaaS teams

Our Latest Work

We strive hard to deliver result-driven digital solutions across the globe. Check out our case studies to get a glimpse of how we ideate, innovate, and create unconventional digital solutions according to the requirements of our clients.

Discover diverse and passionate insights from our tech enthusiasts. We collaborate across various sectors to streamline operations and drive innovation. Explore our rapidly growing collection of articles to see why we’re at the forefront of IT solutions.

The decision to move from Magento to Shopify is one of the most significant replatforming choices an ecommerce business can make. Magento is powerful, but its power comes with...

Accuracy gap is real: Traditional CPG forecasting carries a 25-40% MAPE error rate. AI-powered models bring that down to 8-15%, according to McKinsey research....

Real stories from global leaders who trusted us with their ideas.

Partnering with APPWRK helped us build a compliant and scalable healthcare platform, accelerating our time-to-market by 35%. Their team consistently delivered outstanding work.

Beesers

Digital Healthcare Client

Collaborating with APPWRK, Sportskeeda modernized its platform into a real-time sports engagement ecosystem, enabling seamless content delivery, scalable fan interactions, and high-velocity performance.

Sportskeeda

Sports & Entertainment Partner

Working with APPWRK was effortless. They captured our vision, maintained full compliance, and delivered a digital experience that built trust and elevated how customers interact with our fintech brand.

PayPenny

Fintech Partner

Working with APPWRK gave us confidence in adopting AI responsibly. Their team built a safe, intelligent bot that transformed how we engage with leads and helped us achieve measurable revenue growth.

IFB

AI Transformation Partner

Leveraging APPWRK’s digital expertise, Nemesis launched a scalable, compliant, and safe super app that connects content delivery, real-time communication, and logistics management within a single platform.

The cost to build a BNPL app like Klarna in 2025 typically starts from $35K to $170K, depending on UI/UX complexity, third-party integrations, compliance scope, and backend scalability.

UI/UX design, platform coverage, backend infrastructure, and third-party integrations are the core cost drivers.

Compliance frameworks like PCI DSS, GDPR, and PSD2 must be built in from day one for long-term scalability.

Hidden costs, including cloud hosting, maintenance, legal audits, and marketing, can impact your total budget more than expected.

You’ll learn how platform scope, backend architecture, and legal frameworks shape both cost and development timelines.

Smart founders reduce development spend using cross-platform tools, modular sprint planning, and fintech-specialized global teams.

BNPL monetization works through merchant transaction fees, late payment charges, interest-based installments, and subscription models.

AI-driven risk engines, behavioral analytics, and fraud detection significantly reduce chargebacks, automate identity verification, and optimize lending decisions in real time.

This blog is crafted for CXOs, fintech founders, and digital product leaders exploring the development of a BNPL app like Klarna in 2025. Whether you're leading product strategy, compliance, or engineering delivery, this guide helps you understand the real costs, technical requirements, and compliance considerations behind launching a scalable BNPL platform.If you're evaluating time-to-market, tech stack decisions, or regulatory fit in the fast-evolving BNPL landscape, this guide will equip you to move with confidence and clarity.

Target Market Growth for BNPL: Klarna’s Model in a Scaling Sector

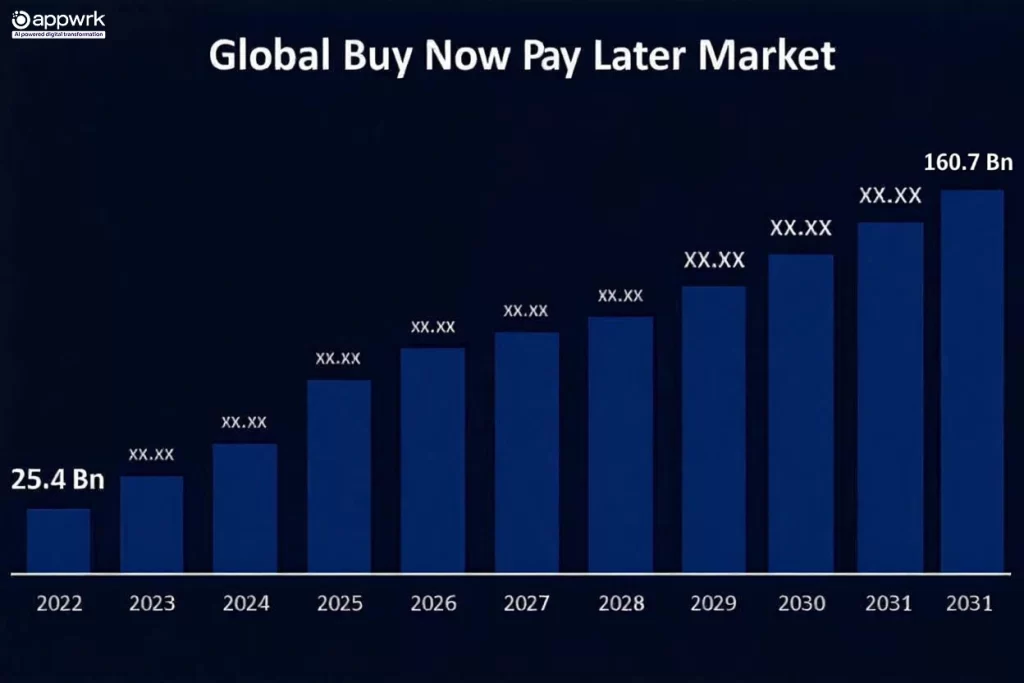

In today’s fast-paced digital economy, consumer expectations are evolving, particularly when it comes to payment flexibility. One of the most notable trends reshaping the retail landscape is the rapid rise of Buy Now, Pay Later (BNPL) services. As more shoppers move online and seek alternative ways to manage their spending, platforms like Klarna are becoming increasingly central to how people shop. According to Statista, global demand for BNPL solutions continues to surge. In the United States alone, the market was valued at approximately $33 billion in 2023, with strong growth projected through 2026 (Statista, U.S. Lending Market).

Klarna is one of the top companies leading this change. It’s based in Sweden and offers people a way to buy items now and pay over time without interest. In its Q3 2024 earnings report, Klarna shared some impressive numbers:

Over 150 million active users

2 million daily transactions

Working with more than 500,000 stores around the world

“The future of payments lies in seamless credit experiences, not plastic cards.” Sebastian Siemiatkowski, CEO, Klarna

For any company planning to develop a BNPL app similar to Klarna, the opportunity is vast and the potential returns are significant. Success depends on executing across four key pillars: intuitive design, seamless payment infrastructure, robust risk management, and strict legal compliance.

The architecture must support scalability and security while delivering a frictionless user journey. Emulating Klarna means taking on the responsibility of building a compliance-driven fintech engine, engineered for trust, transparency, and long-term growth in a regulated environment.

Klarna is a Sweden-based fintech company that has completely transformed the Buy Now Pay Later (BNPL) space. Founded in 2005, the company now operates in more than 45 countries and works with over 500,000 retailers globally. These include major brands like Adidas, H&M, and IKEA. Klarna allows users to make purchases immediately and pay later through smaller, scheduled installments with zero interest. Its focus is on creating digital credit experiences that are simple, secure, and accessible for everyday shoppers.

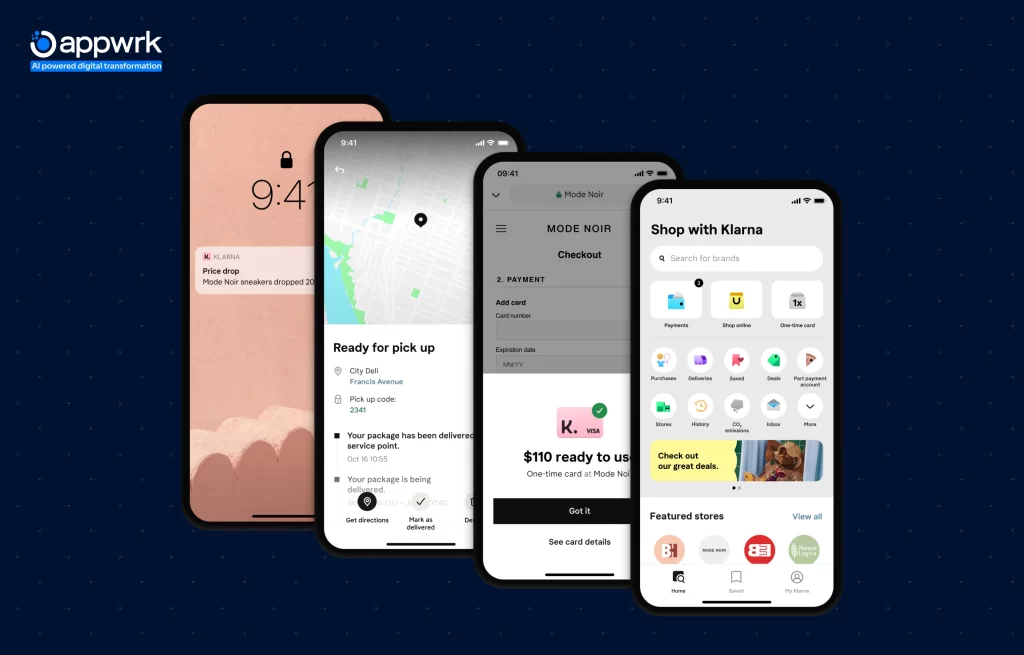

Klarna’s app is a key driver of its success, offering a user-friendly interface that simplifies payments and financial tracking for people of all technical skill levels.

Rating: An impressive 4.6 stars from more than 600,000 users

Top Feedback: Users appreciate the app for its reliable performance, easy navigation, and fast checkout support

How Klarna Helps Users

Klarna’s offerings go beyond delayed payments. It delivers real value by helping users manage their money better while making the shopping process enjoyable.

Splitting Payments into 4 Installments: Users can divide the total cost into four equal, interest-free payments. This makes higher-ticket items more affordable without adding financial pressure.

Smart Budgeting Features: Klarna offers personalized reminders, spending summaries, and due date alerts, encouraging better financial decisions.

Merchant Integration: The app syncs directly with major retailers. That means faster checkout, contextual purchase suggestions, and real-time delivery tracking.

Simple, Trust-Building UI/UX

One of Klarna’s strongest assets is its easy-to-use, trust-building interface. Every screen is crafted to reduce friction and improve clarity, especially for users who aren’t tech-savvy.

Minimalist Design: Klarna uses a clean, distraction-free layout. Users see what matters—payments, tracking, deals, without any clutter.

Personalized Feed: The app tailors promotions and product suggestions based on user behavior, purchase history, and seasonal trends.

One-Tap Navigation: With just a tap, users can manage returns, check payment schedules, and view past orders. No complex menus.

If you want to build a BNPL app, let’s see how much it costs to build a BNPL app like Klarna.

How Much Does It Cost to Build a Buy Now, Pay Later App Like Klarna?

Building a BNPL app like Klarna is not just about coding a payment option. It involves aligning product features with complex fintech workflows, establishing user trust mechanisms, and ensuring cross-border compliance. According to Deloitte, BNPL product development costs scale significantly based on the complexity of user flows, risk automation, compliance layers, and performance expectations in both banking and consumer finance environments.

Estimated Development Ranges

To keep your development budget flexible and founder-friendly, APPWRK structures BNPL app builds into clear stages based on app complexity.

We’ve re-engineered the pricing model to be more efficient than typical market offerings, without compromising on fintech performance.

App Tier

Estimated Cost

Core Features

Time to Build

Essential / Basic

$35,000-$55,000

Includes basic UI for onboarding, streamlined payment flow, and transaction history logging. Integrates with at least one payment gateway like Stripe or PayPal. Offers a functional admin dashboard to give merchants visibility into user activity and payment behaviors.

2-4 months

Growth-Ready

$55,000-$100,000

Modern UI/UX, multi-platform support, APIs, social login, data security layers

This structure allows startups and enterprises to choose a growth path based on budget, compliance load, and target markets, while staying under the standard market pricing.

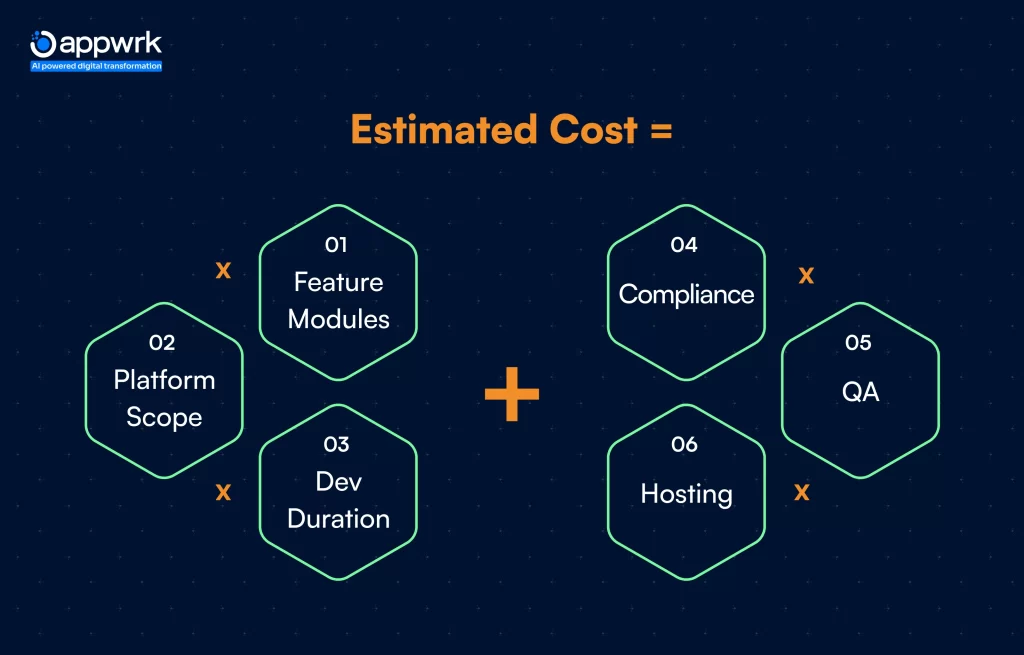

A Simple Formula to Estimate the Cost of Developing a BNPL App

According to the IBM Cloud Architecture Center, estimating the cost to build a BNPL app involves more than just design and development. It must also account for regulatory compliance, hosting infrastructure, and ongoing maintenance to ensure long-term reliability and scalability. Founders of the BNPL app often use a modular formula to get clarity early on.

This simple cost equation gives product owners a high-level understanding of what it takes to launch and scale a Klarna-style BNPL product. Here’s a breakdown of each component:

Feature Modules (10–35 modules) A BNPL app typically includes payment splitting logic, real-time transaction history, user profile settings, admin dashboards, smart notifications, and fraud scoring tools. As the feature count grows, so does the complexity of integration.

Platform Scope Choosing between a single-platform (iOS or Android) or a full-stack app (mobile apps + web-based merchant portal) can double the workload. A cross-platform approach with Flutter or React Native reduces effort but may impact fine-tuned performance.

Development Duration (4–9 months) The build timeline depends on how deep your feature set goes. MVPs with limited features take as little as 4 months, while fully compliant, enterprise-level builds may take up to 9 months, including testing and certifications.

Compliance, Hosting & QA Regulatory measures like PSD2, PCI DSS, and GDPR aren’t optional.QA processesmust also cover usability testing, stress testing, and security audits. Cloud hosting (AWS/GCP) and container orchestration (Docker/Kubernetes) add scalability costs.

This formula is flexible yet realistic for planning a fintech product. It helps budget not just for launch, but also for long-term reliability, audit-readiness, and feature iteration.

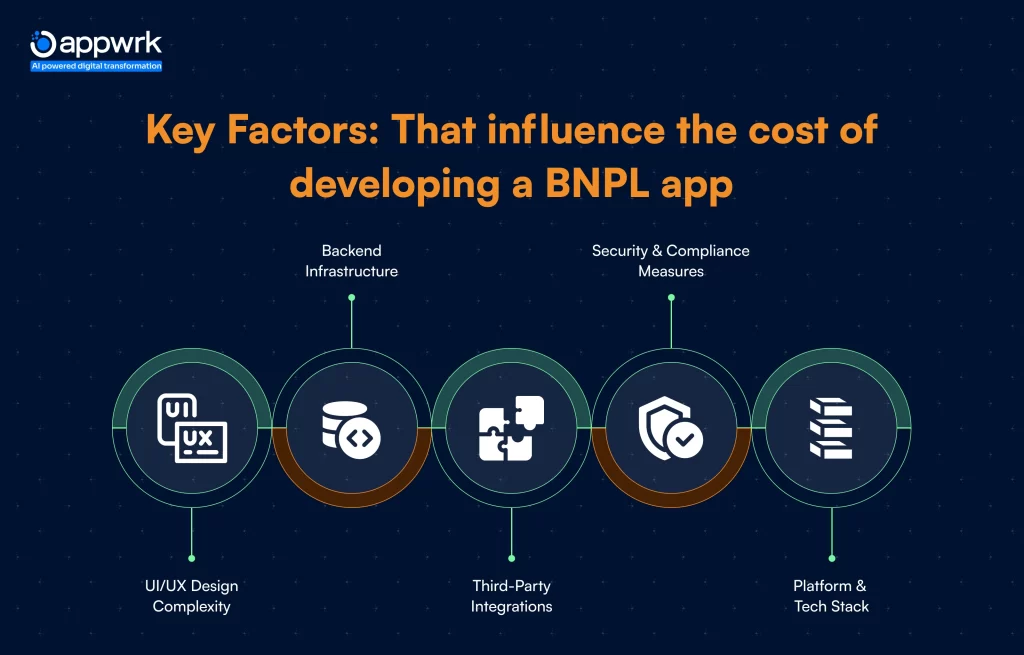

Key Factors That Influence the Cost of Developing a BNPL App

According to insights from a 2025 Gartner Peer Community survey, the cost to build BNPL app is increasingly influenced by platform complexity, consumer protection requirements, and scalability needs. Security layers, regulatory adherence, and user-centric design choices all play a central role. Each decision, from design frameworks to backend orchestration, directly affects both development velocity and cost.

UI/UX Design Complexity

Creating a Klarna-style experience means building dual-sided flows: seamless for users, and data-rich for merchants. The effort goes beyond aesthetics.

Custom Journeys: UI for consumers includes installment breakdowns, alerts, and gamified budgeting. Merchant-side panels focus on payout reports and return analysis.

Micro-Interactions: Subtle animations, swipe feedback, and loading transitions add polish but increase development effort.

Accessibility: Meeting ADA/WCAG standards widens your market and aligns with global app store compliance.

Backend Infrastructure

Your backend isn’t just for managing payments; it’s the BNPL brain that enforces lending logic and syncs user credit across endpoints.

Microservices: Node.js or Java Spring Boot provides modular service handling for users, payments, and fraud.

Real-Time Sync: Kafka pipelines or Firebase real-time DB keep UIs instantly updated across platforms.

Cloud-Native Deployment: Apps built with Docker and orchestrated via Kubernetes scale cost-efficiently across regions like the EU and North America.

Third-Party Integrations

Integrations make your app smart, but they come with license, setup, and latency costs.

KYC/AML Tools: Onfido and Jumio provide instant ID verification and fraud detection.

Payment Gateways: Stripe, Adyen, and Razorpay offer prebuilt checkout kits with API-based pricing models.

Risk Engines: Tools like Alloy, Sift, or LexisNexis help flag suspicious activity and score customer behavior.

Security & Compliance Measures

BNPL apps operate within regulated financial zones, which means compliance is mandatory and not optional.

PCI DSS Level 1: Required for storing or processing credit card data.

GDPR, PSD2, CCPA: Determine how user data is stored and when consent is needed.

The technology stack forms the foundation of your BNPL app, directly influencing development costs, application performance, scalability, and time to market.

Front-End: React Native or Flutter allows cross-platform launch while minimizing code duplication.

Back-End: Node.js for event-based processing or Java Spring Boot for fintech-grade load handling.

Database: Firestore for sync-heavy features; PostgreSQL or MongoDB for flexible querying.

Disclosing the Hidden Cost to Develop a BNPL App

Many startups budget for development and design, but forget the post-launch reality. These hidden costs can quietly drain resources if not planned early on. According to Deloitte, BNPL platforms often face rising operational costs related to user support, compliance maintenance, and marketing retention. These expenses, if overlooked, can grow even faster than the initial development costs.

App Maintenance

After your BNPL app goes live, ongoing updates, operating system compatibility, and user bug reports require monthly investment. Expect costs of $1,500 to $2,000 per month, depending on code complexity and frequency of feature updates.

App Hosting

Reliable hosting for scalable fintech apps means cloud infrastructure. BNPL apps hosted on AWS, GCP, or Azure generally cost $500 to $1,800 monthly, depending on user load, data backup needs, and redundancy planning.

App Marketing & Promotion

Gaining visibility in app stores requires more than just publishing your app. From App Store Optimization (ASO) to paid user acquisition and micro-influencer partnerships, budget at least $8,000 to $45,000 in the initial launch phase for competitive traction.

Legal & Licensing

Operating a BNPL app means navigating a complex web of financial regulations. From getting fintech licenses to data audits and cross-border payment approvals, expect $12,000 to $25,000 in legal costs, especially if expanding internationally.

How To Optimize BNPL App Development Cost

It goes without saying that building a BNPL app involves more than just upfront coding; it’s about making smart decisions that reduce long-term costs and increase efficiency. Businesses that adopt structured planning early on can minimize waste, accelerate time-to-market, and stay flexible as they scale. According to IBM’s IT cost optimization strategies, applying structured frameworks early in the app lifecycle allows teams to reduce waste, prioritize key investments, and maintain agility throughout scaling. As BNPL platforms scale, saving even small amounts early can result in substantial ROI. The key lies in focusing on what matters most: time-to-market, user feedback, and backend efficiency.

Develop an MVP First

Begin by shipping a minimum viable product (MVP) that includes essential BNPL features such as sign-up, product checkout integration, an installment engine, and repayment tracking. This keeps development focused, budgets lean, and lets you validate product-market fit (PMF) faster.

Core Modules: User onboarding, authentication, merchant integration, and simple installment breakdown.

Payment Logic: Installment engine that tracks due amounts and triggers smart notifications.

Early Feedback: Deploy early, collect usage data, and iterate based on real user behaviors.

Prioritize Features

Avoid the trap of feature overload. Many successful BNPL products started with only the essentials, namely payment split, history tracking, and notifications. Build those first, gather traction, and then scale.

Focus Areas: Authentication, merchant payments, user support, and reminders.

Defer Wishlist Items: Delay loyalty programs, AI scoring, or custom reward systems until PMF is achieved.

Cross-Platform Development

Using cross-platform tools like Flutter or React Native can cut development time and cost by up to 50%. You’ll cover both Android and iOS without maintaining two separate codebases.

Single Codebase: Build once and deploy across platforms.

Faster Updates: Update both platforms simultaneously.

Quality doesn’t have to cost a fortune. Hiring skilled developers from regions like India, Eastern Europe, or LATAM can save 40–60% without sacrificing fintech-grade quality.

Global Talent: Many dev shops in these regions specialize in fintech and are experienced with PSD2, PCI DSS, and open banking protocols.

Time Zone Overlap: Structure work hours for daily collaboration.

Transparent Tools: Use Jira, Slack, GitHub for clear deliverables and QA oversight.

ATAM offers world-class fintech dev talent at 40–60%

Must-Have Features to Build a BNPL App Better Than Klarna

If you want to outperform Klarna, it starts with refining the essentials and then layering in value-driving, user-centric features. A well-balanced BNPL product includes fluid UX, useful merchant tools, and technology built for growth.

Payout Scheduling: Automated batch payouts tied to order status and payment completion.

User Side Features

A strong user-side experience is the key to adoption and retention:

Real-Time Balance View: Show active purchases, pending payments, and credit limits clearly.

Delay Repayment Option: Let users request short extensions, automated within policy limits.

Loyalty Points Tracker: Engage returning users with rewards tied to purchase frequency and repayments.

Robust & Scalable Technologies

A BNPL app must be ready to scale and stay secure:

Kubernetes Orchestration: For efficient scaling and zero-downtime deployments.

Node.js with Serverless Functions: Enables real-time response handling while lowering infrastructure costs.

Key Legal and Regulatory Frameworks for BNPL App Development

Before any code is written, legal and compliance readiness must be aligned. BNPL apps deal with sensitive personal and financial data across regulated regions.

Licensing Requirements

BNPL is treated differently across jurisdictions. In some, it’s classified as a credit product and needs a lending license.

Examples: In the U.S., CFPB involvement; in the EU, local credit authorities.

Data Privacy Laws

Handling user information responsibly is core to compliance:

GDPR (Europe), CCPA (California): Govern consent, data usage, and deletion rights.

Consumer Protection Mandates

You must clearly communicate terms, timelines, and resolution mechanisms:

Modern BNPL apps must implement industry-grade security from the start:

PCI DSS: Required if storing or handling credit card info.

ISO 27001: Certifies secure data handling processes and audits.

Real-Time KYC and Fraud Prevention Tools in BNPL App

BNPL apps are attractive targets for fraud due to their low entry barriers and quick credit extensions. A solid fraud prevention strategy must be embedded in both the frontend and backend from day one. According to IBM’s fraud prevention solutions, advanced AI-driven detection tools and real-time behavioral analytics are essential to reduce transaction risk and protect customer data in digital finance environments. Risk engines powered by AI, combined with compliance-grade identity verification, reduce exposure and build trust.

Automated Identity Verification

Protect your platform from identity spoofing and synthetic identity fraud:

Onfido and Jumio: Offer AI-driven document verification, liveness checks, and OCR scanning to validate user identities within seconds. They’re essential for compliant onboarding in regulated regions.

Transaction Risk Analysis

Not all transactions carry the same risk. Real-time analysis helps flag anomalies before they impact your business.

Rules-Based Detection: Create custom rules like flagging high-value transactions from new users or transactions outside a customer’s typical behavior.

ML-Driven Detection: Train machine learning models to score risk based on historical patterns and peer profiles.

Suspicious Behavior Alerts

The app should constantly monitor for indicators of misuse or exploitation.

Session Tracking: Monitor login frequency, session length, and behavior deviation to detect bots or account sharing.

Velocity Checks: Flag rapid multiple sign-ups or payment attempts from the same IP or device.

Step-by-Step Guide to Build an App Like Klarna

Creating a scalable and secure BNPL platform like Klarna involves more than just coding screens. According to McKinsey’s 2025 report on BNPL business models, winning in this space demands precise alignment between business strategy and development execution, especially as the market fragments into niche verticals like healthcare, travel, and B2B commerce. It requires a strategic development journey, from ideation to post-launch iteration, that aligns with user needs and compliance obligations.

Market Research and Target Audience Analysis

Before designing or coding, analyze market trends, user pain points, and spending behavior. Understand competitors like Klarna, Affirm, and Afterpay to identify gaps and opportunities.

Tools: Surveys, Google Trends, Statista data.

Goal: Identify your target niche, whether it’s Gen Z shoppers, B2B merchants, or specialized segments like travel and ticketing payments.

Define App Features and Functionality

Translate insights into a product roadmap. Classify features into “must-haves” (sign-up, payments, KYC) and “differentiators” (cashback, budgeting tools).

Deploy with marketing readiness, analytics hooks, and rollback plans. Keep teams ready for feedback loops.

Monitoring: Sentry, New Relic, Mixpanel.

Iterations: Weekly sprints based on real-world feedback.

Effective Monetization Strategies for an App Like Klarna

A successful BNPL business model earns from both users and merchants while maintaining user trust and regulatory compliance. Klarna, Afterpay, and Affirm follow this dual monetization approach with scalable revenue streams. When building your BNPL app, aligning monetization with transparency and ease of use is critical.

One of the main revenue drivers is the merchant discount rate. BNPL platforms typically charge retailers between 2% to 6% per transaction. This fee covers credit risk, fraud protection, and the convenience of installment-based purchasing, which significantly boosts cart value and conversion rates.

Merchants are often willing to pay a premium if the platform drives higher average order values and repeat purchases.

Late Payment Fees

While Klarna emphasizes interest-free payments, they still apply regulated late fees, usually ranging from $7 to $15 per incident. These fees are carefully disclosed to maintain user transparency and regulatory compliance.

Best Practice: Ensure late fees are capped and communicated upfront.

Keyword Highlights: payment defaults, fintech compliance, user trust, repayment behavior.

Interest on Installments

Some BNPL models offer interest-bearing installment plans for larger purchases or longer payment periods. You can blend interest-free short-term credit with interest-based long-term financing, depending on the purchase context and user credit profile.

Monetization Tip: Offer flexible terms and let users choose between interest-free or extended interest plans.

Advanced users may opt into a subscription-based experience (like Klarna Plus), gaining access to exclusive deals, extended returns, or loyalty multipliers. Monthly plans can range from $4.99 to $9.99 and work well for power users.

Use Case: Power shoppers, travel segments, or merchant-first BNPL platforms.

Keyword Highlights: BNPL user retention, premium features, rewards engine.

This strategic monetization mix enables your BNPL platform to drive sustainable revenue, retain loyal users, and scale profitably, especially when balanced with responsible lending practices and high transparency.

How APPWRK Can Help in BNPL App Development

APPWRK is a trusted mobile app development company with deep expertise in building compliance-driven fintech platforms tailored to regulatory-heavy sectors like BNPL. We focus on scalable architectures, clean UI/UX, and bank-level security protocols that ensure your app performs well under real-world fintech scrutiny.

APPWRK has helped fintech clientsreduce time-to-market by 38% and post-launch churn by 24% using our Agile + Compliance-first approach. With a retention rate of 92%, APPWRK delivers:

Scalable fintech architectures Modular builds that support future growth, currency support, and merchant-side expansion.

Secure payment gateway integrations Integrated with Stripe, Adyen, Razorpay, and PCI-compliant KYC engines like Onfido and Jumio.

MVP roadmapping within 3 weeks We move quickly from product scoping to sprint planning to launch robust MVPs that are built for validation and ready for user feedback.

Dedicated fintech QA and compliance experts Each project is assigned regulatory specialists to ensure GDPR, PSD2, and PCI DSS alignment.

We begin every project with a strategic consultation to understand your goals, regulatory priorities, and tech stack preferences. Then we move into design, development, testing, and deployment, fully aligned with fintech-grade security and business viability.

👉 Connect with us today to accelerate your Klarna-style BNPL app build without blowing your budget.

FAQs

How much time does it take to build a BNPL app like Klarna?

It typically takes 4 to 9 months to develop a BNPL app like Klarna, depending on the scope of features, platform coverage (iOS, Android, Web), and regulatory integrations such as PCI DSS and KYC engines.

What are the essential integrations for a BNPL app?

Key integrations include payment gateways (e.g., Stripe, Adyen), identity verification tools (e.g., Onfido, Jumio), fraud detection systems (e.g., Sift, Alloy), and customer communication tools like CRM or push notification frameworks.

Can I get a custom quote for building my BNPL app idea?

Yes, we offer tailored consultation to scope your app based on your goals, user base, and regulatory needs. Contact us here to get started with a personalized quote.

What’s the first step to validate my BNPL business model?

Start with a no-obligation MVP consultation. We’ll help you prioritize features, plan compliance, and estimate costs. Speak to our fintech experts today.

What compliance does a BNPL app need?

A BNPL platform must meet PCI DSS for payments, GDPR or CCPA for user data privacy, and PSD2 for transaction transparency, especially if operating in Europe or California.

How do BNPL apps like Klarna make money?

BNPL apps generate revenue through merchant commissions (2%-6%), late payment fees, interest-bearing installment plans, and premium subscription tiers with cashback or loyalty perks.

Can I build a BNPL app with React Native?

Yes, React Native is highly recommended for building MVPs and maintaining feature parity across iOS and Android with a single codebase, ideal for cost control and fast market entry.

How to reduce BNPL app development cost?

To cut costs, focus on an MVP-first approach, use open-source modules, adopt cross-platform frameworks, and outsource development to high-quality, cost-effective regions like India or LATAM.

What are the hidden costs in BNPL app development?

Often-overlooked costs include compliance audits, cloud hosting, user acquisition marketing, app store optimization (ASO), and ongoing feature upgrades based on feedback.

Gourav Khanna is the Co-founder and CEO of APPWRK, leading the company’s vision to deliver AI-first, scalable digital solutions for enterprises and high-growth startups. With over 16 years of leadership in technology, he is known for driving digital transformation strategies that connect business ambition with outcome-focused execution across healthcare, retail, logistics, and enterprise operations.

Recognized as a strategic industry voice, Gourav brings deep expertise in product strategy, AI adoption, and platform engineering. Through his insights, he helps decision-makers prioritize market traction, operational efficiency, and long-term ROI while building resilient, user-centric digital systems.

Subscribe to APPWRK Blogs, We'll Do the Rest!

Get Blogs on UI/UX, Mobile Apps, Online Marketing, and Web development technology.

Unlock worthy and priceless suggestions from the masters of mobile and web app development