150+ minds across 4 countries. Join a culture of innovation, ownership & growth.

Rewire for AI

From machine learning to deep learning, from classification tools to overall process automation – our AI engineers will help you retool your existing system or enhance your company results.

Ship faster, scale smarter, built for product companies and SaaS teams

Our Latest Work

We strive hard to deliver result-driven digital solutions across the globe. Check out our case studies to get a glimpse of how we ideate, innovate, and create unconventional digital solutions according to the requirements of our clients.

Discover diverse and passionate insights from our tech enthusiasts. We collaborate across various sectors to streamline operations and drive innovation. Explore our rapidly growing collection of articles to see why we’re at the forefront of IT solutions.

The decision to move from Magento to Shopify is one of the most significant replatforming choices an ecommerce business can make. Magento is powerful, but its power comes with...

Accuracy gap is real: Traditional CPG forecasting carries a 25-40% MAPE error rate. AI-powered models bring that down to 8-15%, according to McKinsey research....

Real stories from global leaders who trusted us with their ideas.

Partnering with APPWRK helped us build a compliant and scalable healthcare platform, accelerating our time-to-market by 35%. Their team consistently delivered outstanding work.

Beesers

Digital Healthcare Client

Collaborating with APPWRK, Sportskeeda modernized its platform into a real-time sports engagement ecosystem, enabling seamless content delivery, scalable fan interactions, and high-velocity performance.

Sportskeeda

Sports & Entertainment Partner

Working with APPWRK was effortless. They captured our vision, maintained full compliance, and delivered a digital experience that built trust and elevated how customers interact with our fintech brand.

PayPenny

Fintech Partner

Working with APPWRK gave us confidence in adopting AI responsibly. Their team built a safe, intelligent bot that transformed how we engage with leads and helped us achieve measurable revenue growth.

IFB

AI Transformation Partner

Leveraging APPWRK’s digital expertise, Nemesis launched a scalable, compliant, and safe super app that connects content delivery, real-time communication, and logistics management within a single platform.

AI fraud detection in banking enables real-time threat identification, behavior-based risk scoring, and automated protection across digital channels. This transformation empowers financial institutions to detect fraud faster, reduce false positives, and improve regulatory compliance.

AI fraud detection is redefining banking security: AI-driven fraud detection leverages real-time risk analytics and anomaly detection to identify threats that traditional systems miss, enabling faster, smarter, and more scalable protection.

Deepfakes and synthetic identities are the new battlegrounds: Banks are deploying AI-powered identity verification, voiceprint analysis, and document forgery detection to tackle deepfake-enabled fraud and manipulated digital identities.

Machine learning models are predicting fraud before it happens: Supervised and unsupervised ML models continuously adapt to evolving fraud behaviors, enabling proactive detection of threats across every banking channel.

AI delivers both operational and compliance efficiency: AI not only reduces fraud losses but also ensures faster, audit-ready responses to regulations like PSD2, AMLD6, and FFIEC guidelines, boosting trust with regulators and customers alike.

Call centers and digital onboarding are getting AI-secured: Banks are now using behavioral analytics, emotion recognition, and voice authentication to secure customer interactions from phishing, account takeover, and verification fraud.

This blog is designed for CISOs, fintech CTOs, fraud prevention officers, banking technology heads, and digital product leaders. It will take you through real-time fraud detection models, emerging threat vectors like deepfakes and phishing, the AI/ML stack transforming fraud operations, and the strategies global financial institutions are using to stay ahead.

AI in Financial Fraud Detection: Market Growth, Trends, and Adoption by Region

With the advent of artificial intelligence and the rise in complex fraud tactics such as synthetic identities, deepfake scams, and real-time account takeovers, financial institutions are overhauling their fraud detection strategies by embedding AI at the core of their security infrastructure. AI-powered systems not only help detect and prevent fraud in real time but also adapt continuously to emerging threats, fueling rapid adoption across global markets and reshaping the future of financial fraud prevention.

The global AI in fintech market size is valued at USD 17.93 billion in 2025, and is expected to reach USD 60.63 billion by 2033, growing at a CAGR of 16.45% during the forecast period (2025-2033). A substantial share of this growth is attributed to banking use cases such as payment fraud detection, transaction monitoring, AML compliance, and biometric verification.

Regional AI Adoption Trends in Banking

North America is leading global adoption, with major banks like JPMorgan and Wells Fargo deploying custom AI stacks to combat account takeovers, payment fraud, and insider threats.

Europe is seeing accelerated growth, driven by PSD2 and GDPR regulations that are increasing demand for explainable AI (XAI) and real-time fraud scoring to ensure regulatory compliance.

Asia-Pacific is scaling rapidly, fueled by a surge in digital transactions across mobile-first economies such as India and Southeast Asia, where AI helps banks manage volume and evolving fraud vectors.

The Middle East & Africa are embracing AI through fintech partnerships, as rising fraud risks push banks to work with AI startups on identity verification, KYC automation, and real-time anomaly detection.

Why This Market Is Exploding

Explosion in digital payment volumes post-COVID.

Global credit card fraud is estimated to reach $43 billion by the end of the year 2026.

Banks are shifting from rule-based systems to adaptive ML models for dynamic fraud response.

Regulators are demanding real-time compliance tracking and auditability.

This rising momentum isn’t just tech-led, but it’s a strategic response to evolving risk patterns and a way to enhance customer trust, fraud resilience, and operational efficiency.

How AI Detects Fraud in Banking Better Than Traditional Systems

The escalating sophistication of financial fraud, ranging from synthetic identities and phishing to real-time social engineering, has exposed the limitations of traditional rule-based detection systems. These legacy frameworks rely on static thresholds and predefined logic, often missing nuanced or novel fraud patterns. In contrast, AI-driven systems leverage machine learning, behavioral analytics, and real-time data to identify anomalies, adapt to emerging threats, and reduce false positives, making them vastly more effective for today’s dynamic risk landscape.

Why Traditional Fraud Detection Systems Are Failing Today

Since the emergence of generative AI and highly automated attack vectors, the fraud landscape has shifted dramatically, exposing critical flaws in traditional detection systems. Designed for simpler, rule-based threats, these legacy tools can’t adapt to sophisticated tactics like deepfake-enabled identity theft, coordinated bot intrusions, or real-time credential abuse.

Why legacy systems fail today:

High false positive rates (up to 85% in some traditional tools).

Inability to recognize multi-channel, multi-device behavior.

Rigid logic fails to catch evolving synthetic identity patterns.

The fraud shift is real: BioCatch reports that synthetic identity fraud accounts for up to 20% of credit losses in neobanks and fintechs.

How AI Replaces Static Rules with Adaptive Fraud Detection

Legacy systems operate on fixed thresholds. AI systems analyze behavioral context, device fingerprinting, time-of-day patterns, and user history, and adjust their logic as patterns evolve.

Key shifts in architecture:

Static fraud rules → Self-learning ML models

Black-box alerts → Explainable AI (XAI) for transparency

This shift reduces false positives by 50-70% while capturing unseen fraud variations across channels.

Best Machine Learning Models Used in Banking Fraud Detection

The backbone of intelligent fraud prevention lies in machine learning diversity:

Supervised Learning It learns from labeled datasets of known fraud and legitimate activity and is highly effective for detecting familiar patterns such as credit card fraud, phishing attempts, and account takeovers.

Unsupervised Learning It excels at uncovering unknown threats by identifying deviations from normal behavior and is ideal for spotting emerging fraud tactics without any historical precedent.

Semi-Supervised & Reinforcement Learning It combines sparse labeled data with continuous learning from real-world interactions and is ideal for dynamic environments like digital onboarding and transaction monitoring, where fraud patterns evolve in real time.

Together, these techniques form a multi-layered defense mechanism that adapts to individual users, fraud vectors, and attack trends.

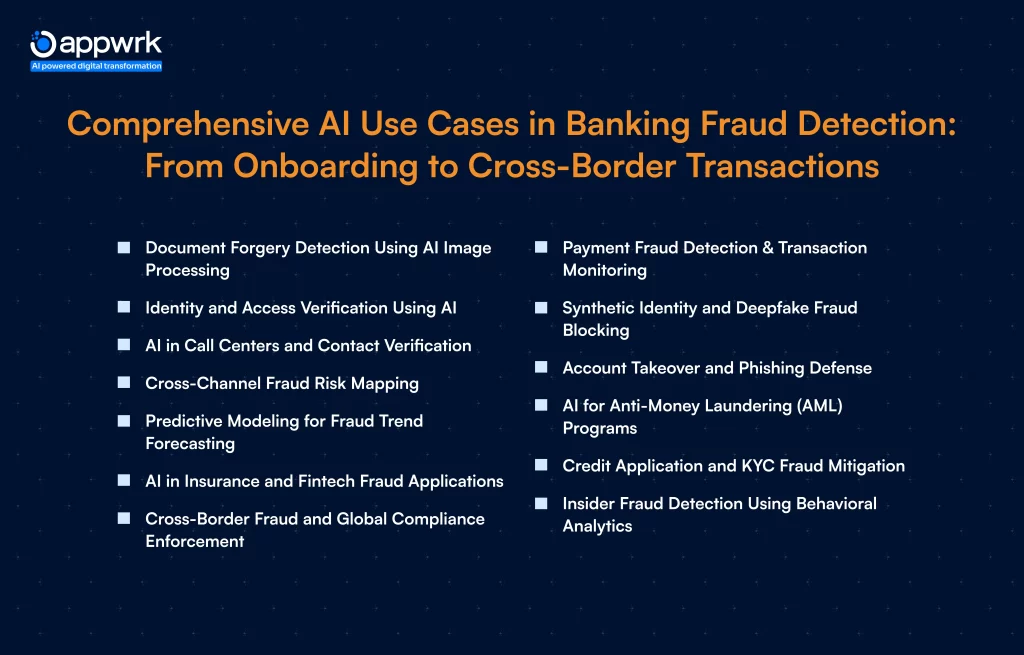

Comprehensive AI Use Cases in Banking Fraud Detection: From Onboarding to Cross-Border Transactions

The use of AI in banking fraud prevention has evolved from single-point transaction flagging to multi-channel risk prediction across the entire customer lifecycle. Financial institutions now deploy AI to monitor everything from the first identity input during onboarding to ongoing transactions across global corridors.

Payment Fraud Detection and Transaction Monitoring

AI systems instantly analyze transaction velocity, geolocation, device fingerprint, and spending behavior to detect anomalies in real-time.

Detect card-not-present fraud.

Block high-risk cross-border transfers.

Flag micro-transaction laundering patterns.

Synthetic Identity and Deepfake Fraud Blocking

AI models can now detect biometric inconsistencies and digital injection attacks used in deepfakes or fake persona creation.

Identify GAN-based facial forgeries.

Detect overlapping identities across banking systems.

Account Takeover and Phishing Defense

AI analyzes subtle behavioral changes such as typing rhythm, login timing, and navigation habits to detect when legitimate credentials are being used by unauthorized users.

Stop credential-stuffing.

Flag man-in-the-middle phishing proxies.

AI for Anti-Money Laundering (AML) Programs

Deep learning enables anomaly detection in massive transaction datasets and reveals hidden entity networks.

Link transactions across shell companies.

Automate SAR (Suspicious Activity Report) triggers.

Credit Application and KYC Fraud Mitigation

AI validates applicant details, historical loan behavior, and identity legitimacy using OCR and multi-bureau triangulation.

Prevent false employment claims.

Detect repeated device/browser fingerprint reuse.

Insider Fraud Detection Using Behavioral Analytics

AI detects internal threats by identifying anomalies in user behavior, such as unusual access times, spikes in data downloads, and deviations from typical workflow patterns, helping flag potential insider fraud early.

Monitor post-shift access spikes.

Track internal device transfers.

Document Forgery Detection Using AI Image Processing

AI image models validate government-issued documents, cheques, and ID photos.

Government ID Tampering

Detect mismatched face contour overlays.

Reveal image manipulation in MRZ (Machine Readable Zone).

Cheque Image Manipulation

Identify altered MICR codes.

Spot duplicate cheque usage across banks.

Identity and Access Verification Using AI

AI strengthens authentication by continuously verifying user identity through contextual signals like device fingerprints, location consistency, behavioral patterns, and biometric cues, ensuring secure access without disrupting the user experience.

Facial and Voice Authentication: Recognize spoofed face prints or AI-generated voice clones.

Device Fingerprinting: Link logins to known browser fingerprints, hardware IDs, and OS versions.

AI-Enhanced Document and Identity Verification: Detects inconsistencies in lighting, DPI noise, hologram placement, and document aging.

AI in Call Centers and Contact Verification

AI leverages voiceprint recognition, speech patterns, and real-time emotion analysis to detect impersonation attempts and flag suspicious calls, enhancing security without compromising customer service speed.

Detect duplicate voiceprints across callers.

Validate the caller’s identity via emotion consistency over time.

Cross-Channel Fraud Risk Mapping

AI connects dots across mobile apps, web logins, ATMs, and in-branch access to create unified fraud risk scoring.

Catch multichannel attack patterns.

Identify pivoting fraud sequences.

Predictive Modeling for Fraud Trend Forecasting

AI models trained on historical fraud data proactively forecast emerging fraud patterns, enabling financial institutions to anticipate and counter next-generation threats before they materialize.

Forecast the seasonality of scam types.

Train systems on synthetic fraud datasets.

AI in Insurance and Fintech Fraud Applications

AI-powered fraud detection frameworks are being seamlessly applied beyond traditional banking, supporting use cases like insurance claims assessment, underwriting automation, and fraud prevention in neobank customer onboarding.

Detect fake claim loops.

Flag overstated income trends.

Cross-Border Fraud and Global Compliance Enforcement

Real-time sanction screening, combined with a cross-jurisdiction rules engine, provides comprehensive regulatory compliance for multinational operations by adapting to diverse and evolving global requirements.

Block transfers to sanctioned regions.

Apply real-time rule changes for FATF/GDPR.

Strategic Business Benefits of AI Fraud Detection in Banking: Accuracy, Trust, and Cost Optimization

As fraud attempts grow more sophisticated, the role of AI in banking fraud prevention transcends threat mitigation. It drives cost efficiencies, compliance automation, and brand trust, offering measurable business outcomes beyond operational security.

AI’s true power in fraud management isn’t just in detection, it’s in transforming operations. This section outlines how AI empowers financial institutions not only to detect fraud but to outperform competitors in the age of digital transformation.

Scalable Accuracy: Detecting Fraud with Precision and Speed

Machine learning algorithms continuously learn from user behavior and fraud patterns to detect anomalies across transaction types and customer profiles. Unlike rule-based models, AI improves over time, minimizing false alarms while increasing fraud precision.

Key Accuracy Gains

3x faster fraud flagging compared to manual methods.

False positive rates reduced by up to 70% in top banks.

Cost Savings from Automation and Fraud Loss Reduction

AI-driven platforms eliminate the need for manual fraud reviews and reduce operational bottlenecks by automating decisions, triage, and documentation.

Operational Optimization Metrics

20-30% reduction in fraud operations team size through AI augmentation.

Decrease in overall fraud losses by 15-25% within the first year.

Banks that combine AI with robotic process automation (RPA) see higher throughput and significant reductions in false decline handling costs.

Regulatory Alignment Through Audit-Ready AI Systems

AI’s ability to log, justify, and explain fraud decisions makes it a natural ally for regulatory compliance teams. Explainable AI (XAI) enhances confidence among auditors and regulators alike.

RegTech Advantages

Uses dynamic risk thresholds and real-time suspicious activity report (SAR) generation in line with AMLD6 and FFIEC compliance standards.

Supports configurable compliance workflows tailored to specific regulatory requirements in different jurisdictions.

Generates machine-readable audit logs with transparent decision trees for full explainability and traceability.

Building Digital Trust and Reducing Churn

Customers today expect seamless security. AI enables banks to prevent fraud in the background, allowing safe transactions without intrusive checks.

Trust Metrics Improved by AI

45% reduction in customer complaints tied to false declines.

Enhanced net promoter scores (NPS) due to faster dispute resolution.

Loyalty uplift in digital-first segments where user experience and security must coexist.

A Mastercard report found that 76% of users prefer brands that use AI to enhance transaction safety without friction.

Real-Time Detection and Preemptive Loss Containment

AI models work in milliseconds to analyze behavior and block suspicious activity before damage occurs, especially in cross-border transactions and instant payment rails.

Real-Time Fraud Mitigation Benefits

Executes AI-driven fraud decisions within 300 milliseconds of transaction initiation.

Proactively blocks high-value transfers and ACH fraud attempts before completion.

Delivers instant alerts to fraud teams and affected customers for immediate response.

Institutions using real-time AI detection saw an average 28% drop in quarterly fraud losses, as per Accenture’s 2023 fraud analytics benchmark.

These benefits collectively position AI not as a cost center but as a core enabler of secure, scalable banking.

AI Technologies Enabling Real-Time, Scalable Fraud Detection in Banking Systems

Modern fraud threats require technologies that operate faster than humans and smarter than static rules. At the core of banking-grade fraud prevention is a modular, AI-powered technology stack, capable of analyzing real-time data, behavioral patterns, and documents across millions of interactions daily.

Machine Learning and Deep Learning: The Heart of AI Fraud Detection

AI fraud detection starts with training machines to understand both fraudulent intent and legitimate behavior. Machine learning (ML) and deep learning (DL) architectures analyze historical and live data to flag inconsistencies across thousands of variables.

Supervised Learning

Models are trained on labeled data (fraud vs legitimate) and deployed for real-time detection of known threats, such as phishing, account takeover, or credit card fraud.

Unsupervised Learning

These models learn from unlabeled data to detect new or rare anomalies. Crucial for zero-day fraud, synthetic identities, and deepfake-aided onboarding.

Supervised models enable 98% accuracy in known attack scenarios, while unsupervised engines are used in 80% of fintech onboarding models to discover new risk patterns.

Behavioral Biometrics and Intelligent Anomaly Detection

AI-driven fraud detection is evolving from static identity checks to dynamic behavioral profiling. Instead of relying solely on who a user claims to be, modern systems evaluate how they interact, flagging even legitimate-looking sessions when behavior deviates from the norm. This approach enhances security by detecting subtle fraud signals that traditional methods often miss.

Data Signals Tracked

Keystroke pressure, typing rhythm, and gesture fluidity.

Voice pitch, emotion signals, and call response delay.

Device orientation and touchscreen pressure patterns.

By continuously learning each user’s typical patterns, AI can detect and block phishing attempts, session hijacking, and insider threats in real time, based on behavior, not just credentials.

Real-Time Risk Scoring and Contextual Monitoring Engines

AI assigns a dynamic fraud score to each event or transaction using hundreds of contextual variables, from device metadata to behavioral context.

Scoring Model Elements

Geo-IP mismatch and device fingerprint analysis.

Session pattern vs historical transaction behavior.

Micro-pattern deviation scoring (e.g., nighttime access from an atypical region).

Dynamic scoring reduces response latency by 85%, allowing banks to flag fraud within 200-300 milliseconds of detection.

NLP and Pattern Recognition for Fraudulent Document and Voice Detection

Natural Language Processing (NLP) and pattern recognition extend AI beyond structured inputs, helping banks assess voice calls, forms, and scanned IDs for hidden fraud signatures.

Where NLP Is Applied

Real-time voice verification in support centers.

Flagging false documents with sentiment, metadata, and image layers.

Parsing customer interactions for intent and stress signals.

Leading banks now use NLP to screen incoming KYC documents and transcripts for indicators like tampered fields or applicant hesitation.

Predictive Modeling and Adaptive Intelligence

AI fraud detection is no longer reactive as it forecasts risk. Predictive models use temporal pattern shifts, velocity changes, and behavior clusters to warn institutions before fraud occurs.

Forecasting Use Cases

Seasonal fraud spikes before holiday loan surges.

Regional risk escalations from mobile-first phishing attacks.

Predictive analytics has reduced high-value fraud attempts by 42% at institutions that combine behavior monitoring with adaptive scoring.

Blockchain and AI Convergence for Immutable Fraud Defense

The convergence of blockchain and AI introduces tamper-proof fraud audit trails and smart contracts that trigger fraud checks automatically.

Key Integrations

Distributed ledgers validate document timestamps and identity claims.

Smart contracts run AI risk checks before executing high-risk payments.

Cross-bank AI collaboratives share anonymized fraud patterns.

AI-blockchain hybrids are being piloted in trade finance and B2B lending ecosystems to fight forgery, duplicate invoicing, and shell account fraud.

AI Fraud Detection vs. Traditional Banking Systems: Performance, Precision, and Risk Intelligence

As fraud becomes faster, more personalized, and more scalable, banks must upgrade from static rules to intelligent, learning-based systems. Traditional fraud detection tools, built on fixed logic, are now outpaced by AI’s behavior-aware, adaptive, and predictive capabilities. Here’s how the two compare across key performance metrics.

Detection Latency and Accuracy: Real-Time AI vs Delayed Manual Systems

Legacy systems typically flag transactions after batch reviews or when predefined thresholds are breached. These delays often allow fraud to occur before intervention. In contrast, AI models run continuous checks across user behavior, device identity, and transaction context, identifying risk within milliseconds.

Performance Breakdown

Traditional: Rule alerts are processed hourly or daily.

AI-Driven: Fraud flagged within 200-300 ms.

Traditional false positives: 60-85%.

AI false positives: 20-35%.

Real-time detection significantly reduces fraud losses in real-time payment networks (RTP, UPI, FedNow) where speed is critical.

Scalability and Automation: AI for Omnichannel Fraud Surveillance

With more customers interacting across apps, ATMs, voice banking, and web, traditional systems lack the scale or agility to manage omnichannel threats. AI-powered engines dynamically analyze millions of signals from various touchpoints in parallel.

AI Scalability Wins:

Horizontal scale across cloud infrastructure.

Real-time processing for mobile and web sessions.

Automation of triage, scoring, and alert workflows.

AI lets digital banks process over 200,000 customer actions per second without analyst bottlenecks.

Static Rules vs. Adaptive Intelligence: Overcoming Pattern Blindness

Rule-based systems only detect threats they are told to look for. AI detects emerging, patternless fraud through anomaly detection, behavior drift tracking, and predictive clustering.

Why Rule-Based Logic Fails:

Unable to detect synthetic identities and deepfake-enabled fraud.

Requires constant manual updates to maintain rule accuracy.

Produces excessive false alerts, leading to alert fatigue and missed real threats.

Self-learning models retrain on live data, spotting subtle deviations that escape rules.

Enhanced Decision Support and Threat Pattern Tracking via AI Models

AI systems go beyond simple transaction flagging by delivering context-aware decision support. They analyze hundreds of real-time signals per session, identify evolving threat patterns, and continuously adapt to the shifting tactics of fraudsters, helping teams make faster, smarter, and more informed decisions.

False Positive Reduction

AI evaluates transaction legitimacy through multi-layered risk scoring, preventing legitimate user blocks that damage the experience.

Results:

Fewer customer complaints.

Improved approval rates.

Better fraud team efficiency.

Threat Evolution Visibility

AI creates maps of fraud vector shifts, tracking how phishing evolves, which devices are reused, and which regions show new threat spikes.

According to Accenture, AI-enabled fraud teams are 35% more responsive to new fraud campaigns, thanks to trend modeling and context awareness.

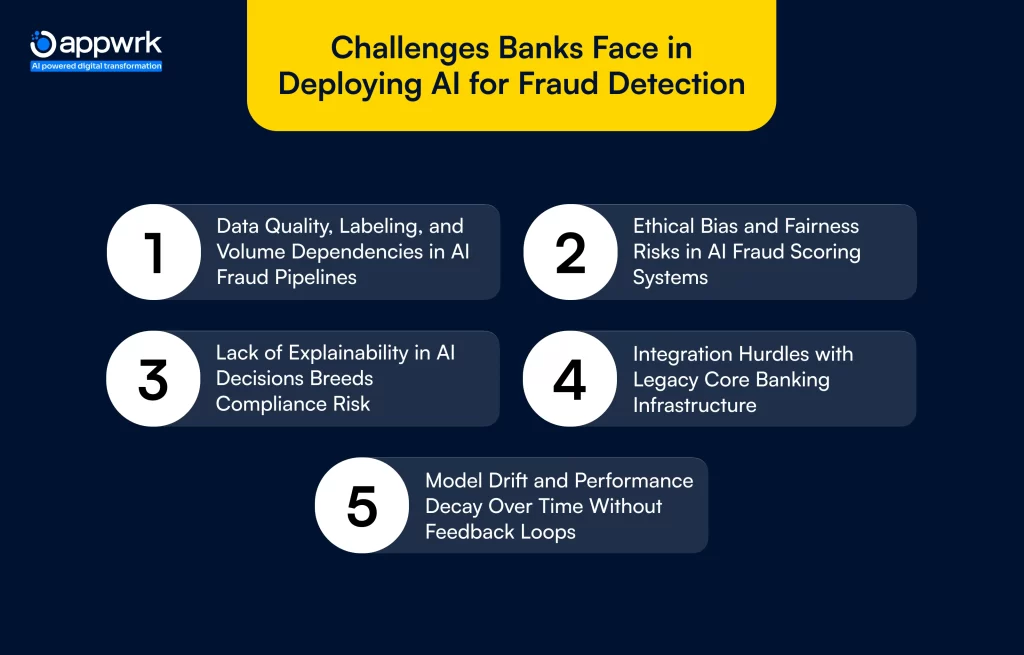

Challenges Banks Face in Deploying AI for Fraud Detection

Despite its immense promise, AI fraud detection in banking comes with real-world hurdles, ranging from poor data infrastructure to compliance risks and model decay. For successful deployment, banks must navigate a spectrum of technical, ethical, and operational roadblocks. Here’s a breakdown of what can go wrong and how to future-proof your AI strategy.

Data Quality, Labeling, and Volume Dependencies in AI Fraud Pipelines

High-quality, labeled data is the fuel of accurate AI fraud detection. But many banks struggle with fragmented databases, inconsistent logging practices, and low volumes of labeled fraud instances.

Structural Data Challenges:

Siloed transaction records across payment, lending, and onboarding systems.

Incomplete metadata, like missing timestamps, device types, or channel indicators.

Manual errors in fraud tagging or delayed fraud confirmation.

Poor data leads to biased learning, noisy predictions, and underperforming fraud detection rates. In fact, model accuracy can drop by 40% or more when trained on poorly structured or unbalanced data.

Ethical Bias and Fairness Risks in AI Fraud Scoring Systems

AI isn’t neutral as it mirrors the data it’s trained on. If the data carries bias, the fraud models will too. This raises serious reputational, legal, and customer trust issues for banks using AI without fairness controls.

Bias Emergence Points:

Over-policing of ZIP codes or device types tied to underserved groups.

Feedback loops reinforcing prior bias (e.g., more fraud labels from high-flag zones).

Banks must embed fairness audits, demographic balancing, and transparency protocols into AI pipelines from day one.

Lack of Explainability in AI Decisions Breeds Compliance Risk

One of the biggest challenges with AI fraud engines is that many operate as black boxes. They offer verdicts without rationale, leaving compliance officers, customers, and regulators in the dark.

Where Explainability is Critical:

Declined loan or flagged payment disputes.

Suspicious Activity Reports (SARs) justification.

GDPR “right to explanation” enforcement in the EU.

The rise of Explainable AI (XAI) frameworks like SHAP, LIME, and RuleFit allows institutions to interpret model logic in auditable, regulator-friendly formats.

Integration Hurdles with Legacy Core Banking Infrastructure

Most legacy banking systems were never built to handle AI’s data demands, resulting in slow deployments, disjointed alerts, and broken fraud intelligence loops.

Batch processing delay due to COB (Close of Business) operations.

Inability to deploy ML models close to core ledgers.

Without native integration, AI models run in silos, missing key behavior context that reduces fraud detection precision.

Model Drift and Performance Decay Over Time Without Feedback Loops

AI models are not static, as they degrade as fraud patterns evolve. New device behaviors, attack vectors, or macroeconomic trends can cause model drift, where accuracy dips silently over time.

Model Decay Catalysts:

Shifting transaction behavior due to fintech adoption.

Increased deepfake usage in onboarding.

Macro-trend events like tax season scams or economic relief fraud.

Robust MLOps (Machine Learning Operations) practices, such as real-time feedback ingestion, A/B testing of new models, and automatic retraining pipelines, can keep fraud detection performance consistent.

How to Build an AI-Powered Fraud Detection Strategy for Banks

Crafting an effective AI fraud detection strategy isn’t just about buying tools; it’s about integrating governance, intelligence, and infrastructure into a unified, resilient, and explainable fraud ecosystem. This section outlines a tactical blueprint for financial institutions to embed AI at the core of their fraud defense stack.

Strategic Framework for AI Adoption in Financial Fraud Defense

Before deploying AI, banks must align fraud use cases with business risk priorities, technology readiness, and regulatory constraints.

Adoption Blueprint Includes:

Use Case Mapping: Prioritize fraud scenarios, e.g., ATO, payment manipulation, onboarding fraud

Risk Profiling: Match fraud vectors to customer segments, regions, and transaction types

Capability Audit: Assess ML maturity, data flow latency, labeling pipelines, and SIEM integrations

Use NIST AI RMF, MITRE ATLAS, and FFIEC CAT to guide your implementation lifecycle across risk, compliance, and response layers.

Governance and Compliance: Making AI Explainable, Ethical, and Auditable

Banks must embed governance frameworks that ensure AI decisions are transparent, unbiased, and legally defensible, especially when denying transactions or blocking accounts.

Governance Stack Includes:

AI Steering Committee with cross-functional representation from fraud, compliance, and risk management to oversee model development and deployment.

Bias Auditing Processes to ensure training data and model outputs are fair, balanced, and equitable across all user segments.

Explainability Frameworks leveraging tools like SHAP or LIME to make AI decisions transparent, interpretable, and regulatory-compliant.

The EU’s AI Act, GDPR, and U.S. FFIEC guidelines mandate documentation of AI model decisions affecting customers.

Defining Key KPIs and ROI Metrics for AI-Powered Fraud Defense

AI fraud detection initiatives must demonstrate business value, not just technical novelty. Make sure you define fraud-specific KPIs and cost savings benchmarks from the start.

ROI Measurement Tactics:

Cost per fraud blocked ($ saved vs $ invested).

Reduction in manual reviews (% of alerts auto-resolved).

False positive rate reduction (%).

Time-to-detection improvement (MTTD).

According to IBM, banks using AI-based fraud detection saw a 60% increase in analyst efficiency and a 25% drop in fraud-related losses within the first 12 months.

Explainable AI (XAI) in Fraud Models: Making AI Decisions Transparent and Defensible

In regulated environments, black-box models won’t pass compliance checks. AI systems must be interpretable, traceable, and logically justifiable.

XAI Design Features:

Visual heatmaps of top fraud signals (e.g., velocity, device mismatch).

Ranked feature contribution to each fraud score.

Case logs for every decision, including override history and retraining references.

XAI enables faster audit resolution and reduces false disputes with customers, building trust and transparency.

Building Scalable Data Architecture and Model Lifecycle Infrastructure

AI fraud detection thrives on real-time, multi-source, high-fidelity data. A modern architecture must support data engineering, model iteration, and scalable deployment.

Core Architecture Layers:

Real-time data ingestion from APIs, CRM, and core banking systems.

Feature stores to standardize fraud variables (e.g., session time, geo-IP).

MLOps pipelines for continuous retraining, monitoring, and rollback.

Use cloud-native or hybrid data stacks to ensure low-latency scoring and scalable model serving.

Enabling Cross-Functional Collaboration for Strategic AI Rollouts

Effective AI deployment requires coordination beyond tech. Cross-functional teams must align around fraud intent, response protocols, and system constraints.

Stakeholder Collaboration Includes:

Fraud Analysts who define fraud typologies, label training data, and validate AI-generated alerts for accuracy and relevance.

Compliance Officers who establish regulatory boundaries, ensure auditability, and align AI models with evolving legal standards.

Engineering Teams that manage model deployment, ensure scalability, and integrate alert systems into operational workflows.

Data Scientists who engineer fraud-relevant features, optimize model performance, and monitor for drift or degradation over time.

Set up a Fraud Intelligence Hub to centralize incident data, AI outcomes, human reviews, and model performance logs.

Next-Gen AI Innovations in Banking Fraud Prevention: Federated Learning, Edge AI & Generative AI Defense

Financial fraud prevention is entering a transformative era, powered by pioneering AI technologies that deliver privacy-first, real-time analytics and GenAI-resistant defenses. These innovations are shaping how banks detect, predict, and combat fraud across channels.

Federated Learning- Privacy-First, Collaborative Fraud Model Training

Federated learning enables financial institutions to train shared fraud detection models collectively without sharing raw customer data. Each bank trains locally and sends only model updates to a central server, preserving data privacy while expanding detection coverage.

Key Advantages:

Leverages cross-institution data to uncover rare fraud patterns.

Complies with GDPR/data residency regulations.

Lowers bias by aggregating diverse datasets.

Edge AI- Real-Time, On‑Device Fraud Detection with Minimal Latency

Deploying AI directly on edge devices, such as mobile phones, ATMs, and point-of-sale terminals, enables real-time fraud detection with near-zero latency. By processing data locally, institutions can instantly flag suspicious activity without relying on cloud connectivity, enhancing both speed and security.

Edge AI Capabilities:

Analyzes biometric and behavioral signals on-device.

Detects anomalies locally, bypassing network lag.

Ensures compliance with regional data sovereignty laws.

Edge-AI enables fraud decisions in under 300 milliseconds, enhancing security and privacy in low-connectivity environments.

Generative AI Threat Detection: Counter-GANs and Authenticity Assurance

Generative models (e.g., GANs, LLMs) are tools of both attackers and defenders. Fraudsters use them for sophisticated deepfakes, but banks are deploying counter-GANs and artifact detection to neutralize threats.

Defense Strategies Include:

Liveness-detection systems coupled with face analytics.

Prompt-response analysis to expose AI-generated content.

Banks integrating these solutions see improved resilience against deepfake ID fraud, though specific ROI studies are still emerging.

Banks are embedding fraud detection into broader security frameworks like SIEM and XDR, enabling unified intelligence across transaction, endpoint, and network domains.

Integration Outcomes:

Fraud risk scores appear in security operations dashboards.

Shared telemetry across identity, fraud, and network systems.

Coordinated responses to hybrid fraud and cyber incidents.

This convergence offers visibility into threats that span digital & physical domains, e.g., phishing coupled with malware or insider collusion.

How Banks Train Customers to Prevent Fraud and Stay Secure Online

Banks strengthen fraud resilience not only by deploying AI, but also by empowering customers as proactive partners in fraud detection. Awareness and engagement strategies amplify protection across channels, combining technology, education, and customer action.

Targeted Awareness Campaigns & Digital Hygiene Training

Proactive customer education reduces risk by informing users about fraud techniques and safe behaviors.

Essential Messaging Includes:

Learn to recognize phishing attempts, fake URLs, and deceptive email addresses.

Regularly update apps and devices to patch vulnerabilities.

Banks with strong customer-awareness programs reported fraud losses decreasing by 20%, according to reports. Additionally, a study on e‑banking fraud awareness in Africa found that limited public knowledge drove higher scam susceptibility.

Timely intel empowers customers to respond instantly.

Alert Features:

Push notifications and SMS that flag unusual transactions like out-of-pattern purchases or logins.

Voice-based alerts using AI agents, enabling immediate confirmation and real-time transaction blocking.

Users respond 35% faster to AI-generated fraud alerts compared to standard notification systems.

Co‑Designed Fraud Reporting & Community Feedback Loops

Bots alone aren’t sufficient. Customer feedback is essential to closing the fraud detection loop.

Customer-First Features:

“Report suspicious activity” buttons or chat support within apps.

Shared phishing feedback, where flagged reports help all users stay alert.

Community-engaged programs decreased repeat phishing incidents by 40%.

Ongoing Customer Engagement via Phishing Simulations & Training

Banks are moving beyond one-off alerts by developing long-term fraud resilience through continuous monitoring, adaptive AI models, and proactive threat mitigation strategies.

Engagement Tools Include:

Periodic phishing simulations are delivered through SMS, email, or app prompts.

Scenario-based quizzes teach users how to respond to suspicious requests.

Engagement boosts customer fraud literacy, reducing susceptibility to fraud campaigns tied to generative AI deepfakes.

Monitoring & Continuous Improvement After AI Fraud System Deployment

Launching an AI fraud model is just the beginning. Banks need a robust monitoring framework, model drift detection, and continuous retraining processes to ensure the system evolves with sophisticated fraud tactics. Below is a structured view of essential maintenance and performance enhancement practices.

AI fraud systems must deliver persistent surveillance and integrate seamlessly with operational workflows:

Live model health dashboards track metrics like inference latency, false positive/negative rates, and overall prediction confidence.

Automated alert triggers activate when drift thresholds are breached, helping fraud teams intervene proactively.

Audit-ready logs capture inputs, decision rationale, and timestamps to support compliance with FFIEC, GDPR, and PSD2 standards.

Banks adopting Amazon SageMaker Model Monitor apply real-time data and concept drift checks to maintain fraud model integrity and regulatory governance.

Human-in-the-Loop Feedback & Pipeline Refinement

AI systems excel with human oversight. Integrating fraud analyst decisions refines models continuously:

Flag validation enables analysts to directly label false positives and false negatives within the system, improving accuracy over time.

Label enrichment feeds confirmed fraud cases back into the training dataset, continuously refining model performance.

Unified pipelines powered by MLOps integrate real-time data, analyst input, and automated retraining to keep fraud models adaptive and current.

Incorporating human feedback significantly boosts fraud detection models’ precision, especially when managing evolving attack vectors.

Ongoing refinement of AI models ensures they remain effective and adaptive, staying ahead of increasingly sophisticated and evolving fraud tactics.

Root-cause investigations dissect fraud failures to detect feature gaps.

Feature engineering cycles introduce new predictors, like behavioral or temporal signals.

A/B testingensures updates preserve or improve performance before full deployment.

This process sharpens the system’s ability to counter emerging fraud tactics swiftly and effectively.

Regional Trends in AI Fraud Detection for Banks and Fintechs

AI adoption in fraud detection is evolving at different speeds across global regions, influenced by local regulations, infrastructure maturity, and scam typologies. From real-time biometric authentication in the US to regulatory AI innovations in Europe and APAC, here’s how different geographies are shaping the AI fraud prevention landscape.

North America: Leading in AI Fraud Detection Infrastructure

North America holds 39% of the global AI fraud detection market ($4.7B), driven by advanced cloud infrastructure, FFIEC/FINCEN regulations, and behavioral analytics.

Real-time AI fraud detection engines are actively deployed by leading US banks to enhance speed and accuracy in threat mitigation

Strong emphasis is placed on model governance and explainability to ensure alignment with regulatory compliance frameworks and audit requirements

Europe & UK: AI Growth Shaped by PSD2 and GDPR

The EU AI fraud market is projected to reach $9.7B by 2025 (17.9% CAGR), propelled by regulation-driven innovation.

AI is used in biometric onboarding and AML flagging.

The UK leads in APP fraud detection via open banking platforms.

Asia-Pacific: Fastest-Growing Region in AI-Driven Fraud Control

Asia-Pacific is leading global growth in AI-powered fraud prevention, driven by rapid digital adoption, mobile-first banking ecosystems, and rising fintech activity across emerging markets.

Real-time anomaly detection, device biometrics

Strong adoption by digital-first banks in India, Singapore, and Australia

MEA & LATAM: Mobile-Led AI Fraud Rollouts Underway

Regions like the UAE, Nigeria, and Brazil are adopting AI for ATM fraud, SIM swaps, and real-time KYC.

AI adoption accelerated through fintech partnerships.

AML systems are now integrated into onboarding processes.

How APPWRK Supports AI-Powered Fraud Detection

APPWRK empowers banks and fintechs with adaptive, AI-driven fraud detection stacks tailored to regional risks and compliance norms. Their approach blends behavioral science, smart automation, and explainability to build agile, regulation-ready fraud defenses.

Multi-Layered AI Fraud Stack for Banks

APPWRK delivers a modular AI platform combining behavioral modeling, biometric analysis, and AML integration.

Smart chatbots for fraud interaction.

Supervised & unsupervised ML pipelines.

Real-time flagging of high-risk events.

Measurable Results from APPWRK Deployments

APPWRK’s AI-driven fraud defense solutions consistently deliver quantifiable value across diverse financial institutions. From streamlining detection workflows to minimizing alert fatigue, our implementations are built for real-world impact.

Here are a few key outcomes from recent deployments:

Lower false positives.

Faster fraud detection.

Scalable fraud rules tailored to institutions.

Why Banks Choose APPWRK for AI Fraud Defense

Banks partner with APPWRK to build intelligent, future-ready fraud prevention systems that scale with evolving threats and regulatory demands. Our solutions combine speed, adaptability, and compliance to deliver enterprise-grade protection.

Modular Architecture– From standalone bot detection to full-scale fraud orchestration, APPWRK’s solutions grow with your needs.

Compliance-First Design– Built-in explainable AI (XAI), detailed audit logs, and pre-mapped regulatory standards like FFIEC, GDPR, and PSD2.

Adaptive Intelligence– Customizable machine learning rules tailored to each bank’s risk profile, transaction volume, and customer behavior.

1. What are the key AI use cases in banking fraud detection? AI is transforming banking fraud detection by powering real-time transaction monitoring, identifying synthetic identities, analyzing behavioral biometrics, and detecting phishing attempts. It supports anti-money laundering (AML), insider fraud detection, and onboarding verification with high precision.

2. How does AI fraud detection support regulatory compliance in banking? AI models are trained to align with financial regulations like PSD2, FFIEC, and FATF. Explainable AI frameworks provide audit-friendly transparency through score attribution, rule tracing, and model explainability, ensuring banks can pass compliance reviews efficiently.

3. Can AI detect real-time fraud attempts like phishing or account takeovers? Yes. AI models analyze behavioral changes such as login anomalies, device mismatches, and session patterns to detect account takeovers, while NLP-based engines flag phishing messages through tone and link analysis, often within milliseconds of attack onset.

4. How does AI reduce false positives in fraud detection systems? Using adaptive models and contextual decision-making, AI distinguishes between legitimate anomalies and real threats. This reduces alert fatigue and ensures investigative teams only act on verified high-risk cases, boosting operational efficiency and fraud catch rates.

5. What is the cost of implementing AI-based fraud detection in banking? The cost of deploying AI fraud detection varies depending on the scale of operations, model complexity, and integration needs with existing systems. Pricing typically accounts for model training, data infrastructure, compliance features, and real-time monitoring capabilities.

Looking for a tailored cost estimate? APPWRK can help you assess the right AI fraud stack based on your budget and compliance goals.

6. What’s the future of AI fraud prevention in digital banking? By 2030, AI will operate as the real-time command layer for fraud control. Banks will use federated learning, edge AI, and generative intelligence to block fraud pre-emptively, while providing seamless, secure experiences across devices and geographies.

Gourav Khanna is the Co-founder and CEO of APPWRK, leading the company’s vision to deliver AI-first, scalable digital solutions for enterprises and high-growth startups. With over 16 years of leadership in technology, he is known for driving digital transformation strategies that connect business ambition with outcome-focused execution across healthcare, retail, logistics, and enterprise operations.

Recognized as a strategic industry voice, Gourav brings deep expertise in product strategy, AI adoption, and platform engineering. Through his insights, he helps decision-makers prioritize market traction, operational efficiency, and long-term ROI while building resilient, user-centric digital systems.

Subscribe to APPWRK Blogs, We'll Do the Rest!

Get Blogs on UI/UX, Mobile Apps, Online Marketing, and Web development technology.

Unlock worthy and priceless suggestions from the masters of mobile and web app development