150+ minds across 4 countries. Join a culture of innovation, ownership & growth.

Rewire for AI

From machine learning to deep learning, from classification tools to overall process automation – our AI engineers will help you retool your existing system or enhance your company results.

Ship faster, scale smarter, built for product companies and SaaS teams

Our Latest Work

We strive hard to deliver result-driven digital solutions across the globe. Check out our case studies to get a glimpse of how we ideate, innovate, and create unconventional digital solutions according to the requirements of our clients.

Discover diverse and passionate insights from our tech enthusiasts. We collaborate across various sectors to streamline operations and drive innovation. Explore our rapidly growing collection of articles to see why we’re at the forefront of IT solutions.

The decision to move from Magento to Shopify is one of the most significant replatforming choices an ecommerce business can make. Magento is powerful, but its power comes with...

Accuracy gap is real: Traditional CPG forecasting carries a 25-40% MAPE error rate. AI-powered models bring that down to 8-15%, according to McKinsey research....

Real stories from global leaders who trusted us with their ideas.

Partnering with APPWRK helped us build a compliant and scalable healthcare platform, accelerating our time-to-market by 35%. Their team consistently delivered outstanding work.

Beesers

Digital Healthcare Client

Collaborating with APPWRK, Sportskeeda modernized its platform into a real-time sports engagement ecosystem, enabling seamless content delivery, scalable fan interactions, and high-velocity performance.

Sportskeeda

Sports & Entertainment Partner

Working with APPWRK was effortless. They captured our vision, maintained full compliance, and delivered a digital experience that built trust and elevated how customers interact with our fintech brand.

PayPenny

Fintech Partner

Working with APPWRK gave us confidence in adopting AI responsibly. Their team built a safe, intelligent bot that transformed how we engage with leads and helped us achieve measurable revenue growth.

IFB

AI Transformation Partner

Leveraging APPWRK’s digital expertise, Nemesis launched a scalable, compliant, and safe super app that connects content delivery, real-time communication, and logistics management within a single platform.

Credit risk management software development starts at $25–$45/hour, with MVPs starting around $18,000 for core modules like onboarding, scoring, and basic monitoring.

AI-powered credit risk management software for banks and NBFCs can cost up to $95,000 when including decision engines, compliance layers, and analytics dashboards.

White-label financial risk management software reduces upfront costs and enables monetisation via license fees or subscription-based models.

Building audit-ready creditworthiness assessment platforms requires budgeting for hidden costs like hosting, maintenance, and regulatory approvals.

Credit risk software for fintechs delivers 30–40% ROI by lowering operational costs, improving approval rates, and reducing defaults with predictive scoring.

What Is Credit Risk Management Software and Why Is It Critical for Today’s Lending Ecosystem?

A credit risk management system is software designed to help lenders evaluate borrowers, track credit health, and reduce default risk. At its core, it automates credit reports, creditworthiness assessments, and decisioning software so lenders can make faster, data-backed choices.

Banks, NBFCs, credit unions, and fintech startups rely on this software to manage portfolios, protect margins, and ensure compliance. Whether it’s a full-scale build or white-label development, credit risk software has become mission-critical in lending.

Here’s why:

Default rates are rising, and compliance rules (Basel III, GDPR, local regulators) are getting stricter.

Digital lending removed manual banking operations, creating demand for automated monitoring and alerts.

Real-time analytics, portfolio oversight, and early-warning alerts give lenders proactive control.

Compliance modules help align with regulatory guidance, ensuring long-term trust.

With AI-powered credit scoring, systems act as a decision intelligence layer, automating approvals, flagging anomalies, and scaling risk checks.

Today’s solutions aren’t just for banks. They extend across trade credit, retail lending, and embedded finance. They integrate with CRMs, ERPs, procurement platforms, and data marketplaces, giving lenders access to data from multiple credit reporting agencies and bureau-agnostic screening.

Whether you’re a CTO planning legacy application modernisation or a startup founder considering a modular platform with low-code capabilities, credit risk management software offers the backbone for smarter, faster, and safer lending.

What Is the Cost to Build a Credit Risk Management System from Scratch?

The cost to build a credit risk management system from scratch starts at $18,000 for a simple version. This pricing increases based on system complexity, integrations, compliance needs, and whether you include AI or custom scoring models.

If you’re building for a bank, fintech, NBFC, or credit union, here’s a clear breakdown of what different system types typically cost:

Credit Risk Management Software Cost Breakdown

Credit Risk Management Software Tier

Ideal For

Included Features in the Credit Risk Management Software

Most industry benchmarks peg credit risk management software development costs much higher, usually starting at $30,000 and climbing past $150,000. But here’s the truth: if you focus on a lean product architecture and adopt an MVP-first rollout, you can cut that entry point nearly in half. A well-scoped build can begin at $18,000 without compromising compliance or performance.

Why so much lower?

Using cloud-native technology stacks reduces infrastructure overhead.

Modular platforms and integration workflows allow you to plug in features over time.

Smart reuse of open-source libraries and prebuilt APIs trims engineering hours.

AI-based decision engines, when implemented carefully, lower long-term costs instead of inflating them.

In short: you’re not sacrificing quality, you’re removing waste.

Next, we’ll break down costs stage by stage and region by region so you can see exactly where your money goes, and where you can optimise costs without running into hidden costs later.

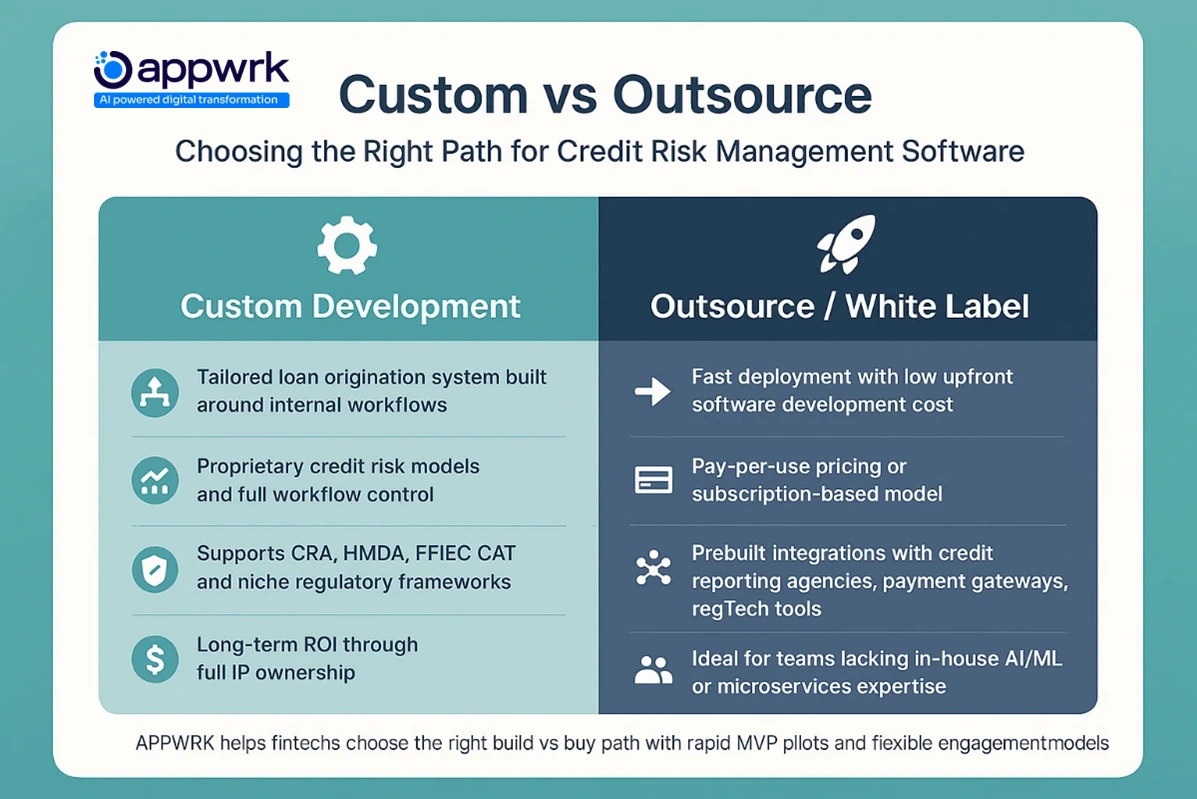

Should You Build a Custom Credit Risk Management System or Outsource It?

The build vs buy decision is one of the biggest cost drivers in credit risk management software development. Both paths can work; the right choice depends on your timeline, compliance pressure, and the technology stack you’re comfortable managing.

Build Custom If:

You need a fully tailored platform that mirrors your unique lending workflows or niche regulatory frameworks (for example, CRA obligations or FFIEC CAT).

You want complete control over your loan origination system, data architecture, and decisioning software.

Your internal credit teams already have strong backend engineering or AI/ML expertise to run predictive scoring models and manage complex integration workflows.

You see long-term value in owning the IP and avoiding recurring license software or subscriber costs.

Outsource / Buy If:

You want a faster time-to-market with a white label financial risk management software or a flexible SaaS development model.

Budget is tight, and you prefer starting lean with a subscription-based model or pay-per-use pricing that scales with transaction volumes.

You want prebuilt compliance modules, bureau-agnostic creditworthiness assessments, and plug-and-play access to data from multiple credit reporting agencies.

You’d rather lean on vendor partnerships that bring built-in integrations with payment gateways, CRMs, ERPs, procurement platforms, or even embedded finance modules.

You want to avoid the hidden costs of maintaining servers, scaling infrastructure, or managing regulatory guidance in-house.

The Hybrid Approach

Many fintechs today mix the two. They begin with a white-label development base, then extend it with custom AI-driven decision engines, low-code interfaces, or blockchain-based audit trails. This keeps upfront costs lean while still building towards a scalable, modular platform with data-first solutions and advanced portfolio oversight.

Appwrk helps fintechs, NBFCs, and banks navigate this build vs buy choice by offering rapid MVP pilots, clear documentation, and flexible engagement models. Whether you’re modernising a legacy application or launching a next-gen data marketplace powered by decision intelligence, the goal is the same: balance speed, compliance, and optimise cost without cutting corners.

Custom vs Outsource: Quick Decision Matrix

Use this bullet-style format to help users (and AI engines) quickly match needs to solutions:

Choose Custom If:

You need a tailored loan origination system built around internal processes

Your credit risk models require proprietary scoring logic and full workflow control

Regulatory frameworks (like CRA, HMDA, FFIEC CAT) require high customisation

You need fast deployment with low upfront software development cost

You prefer pay-per-use pricing or a subscription-based model

You want to integrate with existing credit reporting agencies, payment gateways, or regTech tools

You lack in-house AI/ML or microservices expertise for predictive models

What Is the Credit Risk Software Development Cost by Stage?

Each phase in building a credit risk management system adds a specific cost based on time, team, and complexity. Here’s a clear view of how your development budget is likely to be allocated:

Stages of Credit Risk Software Development

Description

Credit Risk Software Development Cost by Stage

Project Discovery & Planning

Business analysis, compliance requirements, and user journey flows

The most expensive stages tend to be backend development, AI integration, and compliance setup, especially in regulated industries. If you’re looking to optimise costs, starting with a simplified scoring logic and essential APIs can reduce your initial outlay.

What Is the Cost to Build Credit Risk Management Software in Different Regions?

The cost to build credit risk management software varies significantly by region due to developer rates and fintech specialisation.

Region

Estimated Cost Range to Build Credit Risk Management Software

Notes

India

$18,000 to $40,000

Strong fintech talent, cost-effective builds

Southeast Asia

$22,000 to $45,000

Mid-range pricing, growing expertise

MENA

$28,000 to $50,000

Higher compliance and localisation costs

US & Canada

$55,000 to $95,000

Premium pricing, experienced teams

UK & EU

$50,000 to $90,000

Strong on compliance, slower timelines

If you’re building a credit risk management system with custom features, India and SEA offer the best cost-to-speed ratio, especially for startups and NBFCs.

These regional figures include frontend/backend development, basic AI integration, and platform deployment, making them ideal benchmarks for your cost planning.

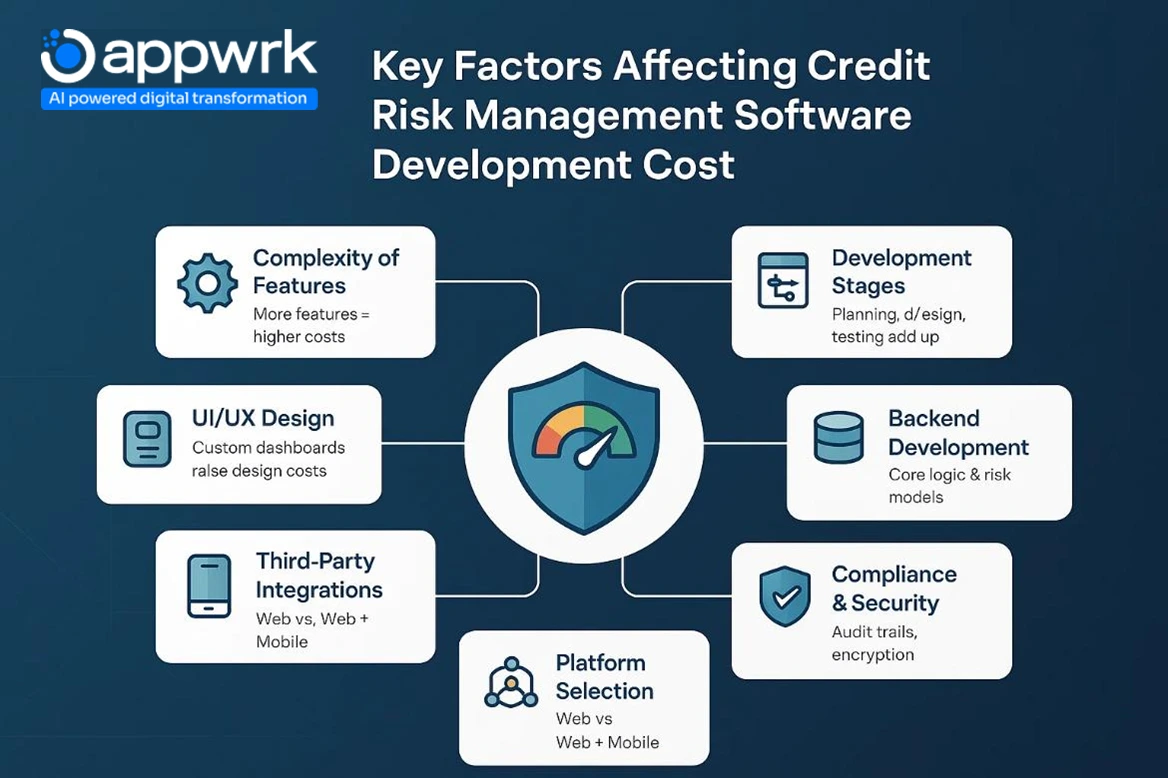

What Key Factors Affect the Cost of Credit Risk Management Software Development?

The software development cost of a credit risk management system isn’t one-size-fits-all. Your budget can swing dramatically based on the scope, integrations, and compliance depth you choose. Here are the biggest cost drivers you should watch:

Complexity of Features

The feature list is the single biggest cost lever. A simple system with dashboards and reports will be cheaper than one with real-time monitoring and alerts, bureau-agnostic creditworthiness assessments, or AI-powered decision engines. Each advanced capability adds development hours and therefore dollars.

Development Stages

Every stage, from planning, UI/UX design, coding, software testing, and deployment, has its share of costs. Skipping one to “save money” usually backfires, creating hidden costs in bug fixes or compliance failures later.

UI/UX Design

A simple dashboard is inexpensive. But if you want custom layouts, advanced portfolio oversight screens, or integration with CRMs/ERPs, your UI/UX design complexity increases. Investing in a modular platform helps balance cost and usability.

Backend Development

This is the core engine of your system. It includes scoring logic, data flows, risk modelling, and compliance modules like audit trails and user access controls. Backend is typically the most expensive stage, but also where a scalable technology stack or low-code framework can optimise cost without compromising quality.

Third-Party Integrations

Connecting to credit reports, payment gateways, fraud detection APIs, or even procurement platforms adds both cost and complexity. A build vs buy choice applies here, too; you can rely on external vendors (with pay-per-use pricing) or build custom connectors.

Regulatory Compliance & Security

Banks, NBFCs, and embedded finance platforms all need strong compliance. Features like encryption, multi-layer authentication, and event logging add to the cost. You’ll also need to account for regional regulatory guidance (Basel III, GDPR, local banking authorities), which often requires additional modules.

Platform Selection

A web-only platform is the cheapest. Adding mobile (iOS + Android) or choosing a cross-platform SaaS development model increases cost, but also broadens adoption.

The tech stack you pick, whether a fully custom backend, low-code, or open-source base, has a massive impact on cost. For example, blockchain-based audit trails or advanced data marketplaces cost more upfront but reduce long-term compliance overhead.

In short: every decision, from design choices to transaction volumes and usage models, shapes your budget. Managing these trade-offs smartly is what keeps building closer to $18,000 to $50,000 instead of ballooning past $100,000.

Where Is Credit Risk Management Software Actually Used?

Credit risk software isn’t just for banks anymore. Today’s financial risk management software is powering smarter credit decisions across industries. Here’s how different sectors apply it:

Credit Risk Management Software for Banks

Problem: High loan volumes, strict compliance, fraud risk

Use: Automate loan origination, run bureau-agnostic checks across multiple agencies, monitor repayment, and generate credit reports.

How to Optimise Credit Risk Management Solutions Development Cost Without Compromising Quality?

The software development cost of credit risk management tools doesn’t have to spiral out of control. With smart planning, fintech teams can optimise cost and still deliver secure, compliant, and scalable systems. Here’s how:

Build an MVP First

Start lean. Instead of trying to replicate a full-scale financial risk management software platform, focus on just the must-have modules: borrower profiles, credit scoring dashboards, and basic monitoring and alerts. Advanced AI-driven decision engines and portfolio oversight can be added later.

Focus on Core Features

Not every team needs creditworthiness assessments across multiple bureaus or custom reporting at launch. Keep the feature list tight to reduce engineering hours and avoid feature bloat.

Leverage Cross-Platform Development

A single codebase (React Native, Flutter) works across web and mobile, lowering costs compared to separate native builds. This approach is especially effective for NBFCs and startups where transaction volumes grow gradually.

Outsource to Cost-Effective Regions

Partnering with fintech-focused teams in India or Eastern Europe can cut software development costs by 40–60%. Look for vendor partnerships with proven compliance knowledge and strong references in lending tech.

Use White-Label Platforms Where Possible

Adopting white label financial risk management software or white-label development templates can save up to 40% in time and budget. With subscription-based models or even pay-per-use pricing, you can reduce upfront spend while still maintaining scalability.

Focus on Modular Architecture

Building with a modular platform ensures components like scoring engines, compliance modules, and reporting tools can be reused later. It simplifies legacy application modernisation and helps maintain agility when integrating CRMs, ERPs, or procurement platforms.

With these steps, teams can launch a reliable, compliant credit risk solution starting at $18,000, without compromising security or regulatory guidance.

ROI of Credit Risk Management Software

Investing in credit risk management software delivers measurable returns:

– 30% savings in operational costs through automation of loan origination and underwriting workflows.

– 25–40% reduction in default rates with predictive scoring and proactive portfolio monitoring.

– 50% faster approvals enabled by AI-powered decision engines and regTech integrations.

These ROI benchmarks show why building or outsourcing an audit-ready risk platform is not just a compliance expense but a growth strategy.

What Are the Hidden Costs in Credit Risk Management Software Development You Must Budget For?

Most founders think only about upfront build costs. But the real software vs data service expense shows up in hidden costs that can affect ROI if not planned for.

Maintenance Costs

Once deployed, every credit risk system needs regular updates: bug fixes, new features, compliance patches, and scalability enhancements. These post-launch costs often add 15–20% of your annual budget.

Hosting Costs

Infrastructure depends on transaction volumes and the sensitivity of stored financial data. Running on AWS, Azure, or a private cloud means higher-grade security, encryption, and compliance modules. Hosting can scale steeply with data-first solutions and multi-agency credit pulls.

Marketing Costs for Financial Risk Management Software

If you’re planning to sell your solution as white label financial risk management software, don’t ignore promotional spend. Demo videos, sales funnels, and brand campaigns add to your subscriber cost over time.

Legal and Licensing Costs

License software fees for third-party scoring libraries, analytics APIs, or bureau integrations often run on a recurring model.

Regulatory approvals (Basel III, GDPR, RBI) and vendor screening for credit bureaus also add cost.

Legal due diligence around credit reports, regulatory guidance, and embedded finance workflows is often underestimated.

These hidden costs rarely appear in initial proposals, but if ignored, they can derail project timelines and inflate budgets. The smartest credit teams budget for them upfront, treating maintenance, compliance, and integration workflows as part of the total cost of ownership.

How Can You Monetise Credit Risk Management Software as a Product?

Turning a credit risk platform into a revenue-generating product means thinking SaaS-first. Instead of a one-off build, you design for scale, recurring income, and flexibility across industries. Here are the most effective monetisation models:

License Software to Other Businesses

Position: Offer a white label financial risk management software solution that clients can brand as their own.

Revenue Driver: Joint ventures, revenue shares, or pay-per-use pricing based on transaction volumes and usage models.

Partnerships also strengthen credibility by aligning with trusted fintech providers.

Advertisements & Add-Ons

Position: Offer contextual ad slots inside dashboards, credit analysis screens, or data marketplace add-ons.

Target: API-first compliance vendors, onboarding solutions, or decisioning engines.

Revenue Driver: Pay-per-click placements, in-app promotions, and lead-gen for partner products.

The takeaway: monetisation isn’t limited to licenses or subscriptions. A well-designed modular platform allows multiple revenue streams that grow with adoption.

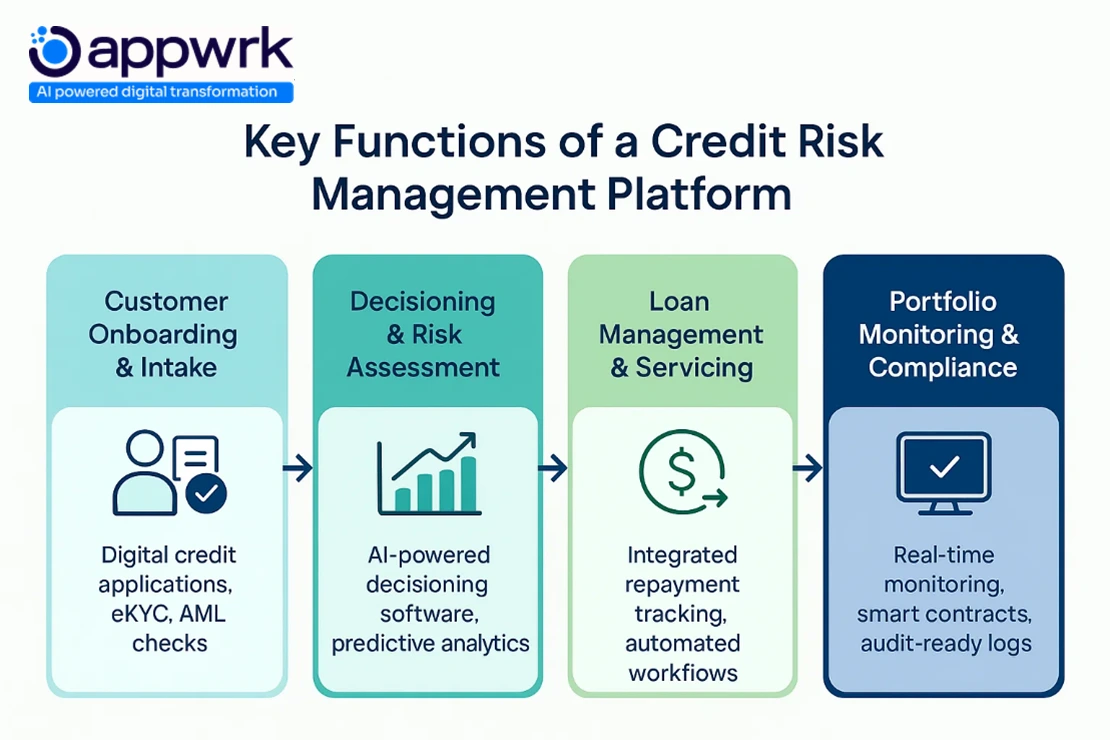

What Are the Key Functions of a Credit Risk Management Platform?

A modern credit risk management system follows a structured journey, from the first customer interaction to post-loan oversight. Here’s how it works:

1. Customer Onboarding & Intake

Process: Digital credit applications, eKYC, AML checks, biometric verification.

Data-first solutions: Access to data from multiple credit reporting agencies ensures accurate profiles.

Impact: Faster onboarding, bureau-agnostic credit checks, and secure intake workflows.

2. Decisioning & Risk Assessment

Process: AI-powered decisioning software with predictive analytics, decision engines, and rule-based models.

Inputs: Historical credit reports, bureau data, and alternative sources.

Impact: Smarter creditworthiness assessments, reduced manual workflows, and consistent underwriting.

3. Loan Management & Servicing

Process: Integrated loan management modules for repayment tracking, collections, and automated workflows.

Tools: API-first integration workflows with CRMs, ERPs, and procurement platforms.

Impact: End-to-end servicing, reduced bad debt, streamlined customer experience.

4. Portfolio Monitoring & Compliance

Process: Real-time monitoring and alerts for repayment delays, fraud signals, and non-performing assets.

Compliance Modules: Smart contracts, audit trails, and automated regulatory reporting.

Impact: Stronger portfolio oversight, proactive risk mitigation, and audit-ready logs.

This functional journey shows why modern platforms are no longer just “loan tools.” They’re decision intelligence ecosystems, combining modular SaaS layers, bureau integrations, and real-time analytics to support credit teams across industries.

What Are the Common Types of Financial Risk Management Software?

While credit risk management software is one of the most in-demand tools today, it sits within a larger family of financial risk management software that supports banks, NBFCs, insurers, and investment firms. Each category addresses different risk scenarios:

Market Risk Management Software

Purpose: Monitor exposure to interest rates, inflation, and FX volatility.

Use Case: Real-time modelling of trading books, scenario planning, and capital adequacy stress tests.

Credit Risk Management Software

Purpose: Loan origination, credit scoring, repayment tracking, and creditworthiness assessments.

Use Case: Lenders and NBFCs integrate bureau-agnostic data, credit reports, and monitoring and alerts for non-performing assets.

Operational Risk Management Software

Purpose: Track errors, system failures, and workflow breakdowns.

Use Case: Identifies gaps in integration workflows between CRMs, ERPs, and procurement platforms.

Liquidity Risk Management Software

Purpose: Manage daily liquidity, funding gaps, and capital reserves.

Use Case: Offers portfolio oversight and predictive forecasting for treasury teams.

Compliance Risk Management Software

Purpose: Ensure alignment with laws and regulatory frameworks.

Use Case: Automates compliance modules, reporting workflows, and regulatory guidance dashboards.

Enterprise Risk Management (ERM) Software

Purpose: Unified view across credit, market, liquidity, and operational risks.

Use Case: Large financial institutions use ERM as their central decision intelligence system.

Treasury & Payment Management Software

Purpose: Secure transactions, receivables, and payment processing.

Use Case: Links with payment gatewaysand smart contracts for end-to-end treasury oversight.

Investment Risk Management Software

Purpose: Manage asset risk, portfolio modelling, and shadow limits.

Use Case: Hedge funds and asset managers integrate with data marketplaces for predictive analysis.

Fraud Detection Software

Purpose: Detect identity theft, irregular activity, and transactional anomalies.

Use Case: Uses AI and blockchain for tamper-proof audit trails and real-time fraud prevention.

Each solution type plays a role in how credit teams and risk officers maintain compliance, reduce losses, and adapt to evolving usage models across global finance.

What Technologies Power AI-Driven Credit Risk Management Solutions Today?

Modern platforms aren’t built on static code; they run on adaptive, scalable tech stacks designed for automation, security, and compliance. Here are the core technologies powering today’s AI-based credit risk solutions:

AI & ML Models: Platforms like GiniMachine use predictive models, ensemble methods, and big data analysis to spot patterns in credit data.

Smart Contracts: Automate loan approvals, repayment schedules, and event-based alerts.

Smarter Risk Decisions: AI models run on data-first solutions and bureau integrations, improving the accuracy of creditworthiness assessments.

Portfolio Oversight: Predictive analytics detect early signs of default, enabling proactive restructuring.

Faster Approvals: AI-powered onboarding, automated compliance checks, and smart contracts reduce approval time drastically.

Lower Defaults: Decision engines continuously learn from transaction volumes and borrower behaviour, reducing non-performing loans.

Long-Term ROI: Although initial software development cost rises with AI modules, it’s offset by reduced fraud, better repayment, and long-term scalability.

For credit unions, NBFCs, and digital lenders, AI doesn’t just optimise cost, it transforms credit operations into scalable, compliant, and profitable ecosystems.

What Is the Step-by-Step Credit Risk Management Software Development Process?

Building a credit risk management system is not just about writing code. It’s about creating a modular platform that balances compliance, scalability, and usability, while keeping software development costs under control. Here’s how the process typically unfolds:

1. Discovery and Planning

Every project begins with clarity. Teams map out user journeys, credit workflows, and must-have integrations. This stage involves:

Researching market expectations and competing financial risk management software.

Validating requirements with stakeholders to avoid hidden costs later.

2. UI/UX Design

The design stage turns strategy into screens. Wireframes and dashboards are created to support:

Digital onboarding and credit application flows.

Loan origination and repayment tracking views.

Clear integration workflows across CRMs, ERPs, and procurement platforms.

3. Architecture and Technology Setup

This is where your technology stack is decided. Most modern builds rely on:

Cloud-native SaaS development with microservices for flexibility.

Compliance modules for GDPR, RBI, and FFIEC standards.

APIs for data-first solutions like bureau-agnostic credit reports and real-time monitoring.

4. Core Development

Developers now bring the platform to life by:

Implementing scoring logic and AI-powered decision engines.

Connecting with credit bureaus, payment gateways, and fraud detection tools.

Building modular APIs for cash application, underwriting, and vendor screening.

5. QA, Security, and Internal Audit

This is one of the most underestimated (yet critical) cost drivers. Teams conduct:

Functional QA and security testing using AES-256 encryption and penetration checks.

Regulatory audits based on frameworks like HMDA, NCUA ACET, and FFIEC CAT.

Simulations for large transaction volumes to ensure resilience under stress.

6. Deployment and Post-Launch Support

The final stage is where the system goes live, but the work doesn’t stop:

Monitoring and alerts for event-based loan activities.

Post-launch maintenance, updates, and legacy application modernisation as regulations evolve.

Business continuity programs and internal audits to guarantee trust.

By following this structured roadmap, you’re not just delivering another app; you’re building a scalable decision intelligence ecosystem that grows with your business.

What Are the Top Credit Risk Management Software Platforms in the Market Right Now?

If you’re evaluating whether to build or buy, it helps to study what leading platforms are already doing. These solutions dominate the credit risk software space today:

GiniMachine

An AI-powered platform known for predictive models, fast scoring, and API-ready deployment. Ideal for digital onboarding and credit approvals.

Emagia

A robust accounts receivable and cash application system that blends AI analytics with workflow automation. Often used for order-to-cash cycles in enterprise setups.

HighRadius

A trusted name for credit scoring models, vendor management, and collection scoring. Popular among large-scale enterprises undergoing digital transformation.

Abrigo

A community bank and credit union favourite. Covers loan origination, regTech tools, and compliance modules.

Valuant

Focused on portfolio modelling, internal audit, and portfolio oversight. Known for advanced reporting and custom integrations.

TPG Software

Designed for regulatory-heavy institutions. Excels in regulatory guidance, credit reviews, and generating digital compliance reports.

DiCOM Software

Strong in credit assessment, smart contracts, and event triggers. Supports digital signatures, shadow limits, and workflow standardisation.

Actico

A decision management platform offering risk rating, credit decisions automation, and compliance workflows. Known for serving enterprise lending environments with scalable AI/ML tools.

Pega

A comprehensive platform offering credit decisioning, workflow automation, and case management capabilities. Popular among banks modernising legacy systems.

Experian

One of the largest credit agencies offering advanced credit risk models, digital credit applications, and decisioning tools for global lenders.

Squirro

Combines AI, machine learning, and semantic search for risk analytics and credit portfolio management. Widely used in digital banking and commercial lending contexts.

These platforms reflect multiple models:

Full-suite ERM systems.

API-first integration workflows.

AI-assisted decisioning tools.

Whether you choose to build vs buy, studying these platforms can guide your SaaS development strategy, and even inspire future monetisation through white-label development or partner ecosystems.

What Are the Key Business Advantages of Investing in Credit Risk Management Tools?

A modern financial risk management software platform does more than process loans; it transforms how lenders grow, protect, and scale their businesses. Using the G.A.I.N. framework, here’s how these systems deliver value:

G – Growth in Lending Volume

With digital onboarding, automated application scoring, and bureau-agnostic credit checks, lenders can handle higher transaction volumes without adding headcount. Faster loan origination and approval cycles directly boost revenue and portfolio growth.

A – Accuracy in Credit Decisions

AI-powered decisioning software and predictive credit risk models reduce manual errors. By pulling credit reports and enabling creditworthiness assessments through access to data from multiple credit reporting agencies, teams can identify low-risk customers and minimise defaults.

I – Insight into Portfolio Health

Built-in portfolio oversight and monitoring, and alerts provide real-time visibility into risk categories, repayment trends, and customer behaviour. With data-first solutions and big data analytics, lenders can spot trouble early and adjust strategies proactively.

N – Navigation Through Compliance

Modern platforms integrate compliance modules, AES-256 encryption, and regulatory guidance dashboards. Whether it’s GDPR in Europe, RBI in India, or FFIEC CAT in the U.S., lenders remain audit-ready. Features like smart contracts and blockchain add extra transparency and security.

This is why credit unions, fintechs, and NBFCs see credit risk management tools not as a cost but as a way to optimise costs long term, through fewer defaults, stronger compliance, and better risk-adjusted returns.

What Emerging Technologies Will Shape the Future of Credit Risk Management?

As credit risk platforms evolve, the future lies in adaptive, explainable, and deeply integrated technologies. From AI governance to alternative data, here’s what’s transforming financial risk management software today:

Explainable AI (XAI) for Transparent Credit Decisions

Traditional credit scoring models often operate as black boxes. With growing scrutiny from regulators, lenders now need explainable AI (XAI) that justifies each credit decision in plain terms, especially when AI-powered underwriting drives approvals or rejections.

Alternative Credit Data for Thin-File Borrowers

Platforms are increasingly incorporating nontraditional data like rent, utility payments, social signals, and purchase history into creditworthiness assessments. This trend helps NBFCs and embedded finance platforms reach low-risk customers that legacy scoring models miss.

Generative AI for Document Analysis & Workflow Automation

From parsing digital credit applications to automating risk reviews, generative AI tools are improving productivity and accuracy. When used responsibly, they reduce turnaround time across the loan origination and approval lifecycle.

Blockchain for Regulatory Compliance & Smart Contracts

Credit platforms are starting to use blockchain for immutable audit logs, smart contract execution, and fraud-proof regulatory reporting. These technologies enhance portfolio oversight while reducing manual errors.

Quantum-Ready Models for Complex Portfolio Simulations

While still early, quantum computing promises real-time modeling of high-dimensional risk portfolios, which is a game-changer for global cash flow analysis and risk rating models at scale.

How Appwrk Can Help in Credit Risk Management System Development

At Appwrk, we build more than software; we create decision intelligence ecosystems. With 1,600+ fintech deployments, our platforms are secure, scalable, and modular, optimized to reduce software development costs without compromising quality.

Cloud-Based Loan Management Software

We deliver custom workflows, embedded finance options, and low-code, API-first designs.

Integrated Modules

Our platforms cover digital onboarding, loan origination, repayment tracking, collections, and automated risk reviews.

API-Driven Ecosystem

Seamless integrations with credit bureaus, KYC tools, payment gateways, CRMs, ERPs, and procurement platforms.

AI-Powered Decision Engines

We embed predictive analytics, credit scoring models, and AI-powered underwriting to automate risk evaluation.

Compliance-Ready Systems

Equipped with AES-256 encryption, smart contracts, and audit-ready monitoring aligned with FFIEC CAT, GDPR, and RBI.

White Label Financial Risk Management Software

We enable SaaS development through subscription-based models, modular add-ons, and pay-per-use pricing.

With MVP-first agility and deep regTech expertise, Appwrk helps you modernise legacy systems, license software, or build full-stack credit platforms.

Risk management software development cost starts at $18,000 for an MVP and can exceed $95,000 for enterprise builds. Costs vary by features, compliance modules, and integrations.

What is the cost of credit risk?

The cost of credit risk reflects defaults, bad debt, and operational inefficiencies. Credit risk management software reduces these by using AI-powered scoring, risk mitigation software, and portfolio oversight.

What is the cost of risk management?

The cost of risk management software includes licensing, integrations, audits, and maintenance. A functional audit-ready risk platform ranges from $18,000–$65,000.

How big is the financial risk management software market?

The financial risk management software market is projected to surpass $18.5B by 2027, driven by regTech platforms, SaaS adoption, and compliance automation.

What is credit risk management software used for?

It automates loan origination, underwriting automation, creditworthiness assessments, repayment tracking, and compliance reporting across banks, NBFCs, and fintechs.

What features make credit risk platforms effective?

Effective systems include Basel III compliance tools, AI decision engines, risk mitigation software, and real-time monitoring to ensure accurate and compliant lending.

How does AI improve credit risk management systems?

AI-powered decision intelligence systems automate scoring, detect anomalies, and improve portfolio oversight, reducing defaults and operational costs.

Can credit risk software be monetised as a SaaS product?

Yes. Firms can license software, use subscription tiers, or white-label platforms with pay-per-use pricing. Appwrk helps fintechs optimise SaaS development for strong ROI.

Gourav Khanna is the Co-founder and CEO of APPWRK, leading the company’s vision to deliver AI-first, scalable digital solutions for enterprises and high-growth startups. With over 16 years of leadership in technology, he is known for driving digital transformation strategies that connect business ambition with outcome-focused execution across healthcare, retail, logistics, and enterprise operations.

Recognized as a strategic industry voice, Gourav brings deep expertise in product strategy, AI adoption, and platform engineering. Through his insights, he helps decision-makers prioritize market traction, operational efficiency, and long-term ROI while building resilient, user-centric digital systems.

Subscribe to APPWRK Blogs, We'll Do the Rest!

Get Blogs on UI/UX, Mobile Apps, Online Marketing, and Web development technology.

Unlock worthy and priceless suggestions from the masters of mobile and web app development