150+ minds across 4 countries. Join a culture of innovation, ownership & growth.

Rewire for AI

From machine learning to deep learning, from classification tools to overall process automation – our AI engineers will help you retool your existing system or enhance your company results.

Ship faster, scale smarter, built for product companies and SaaS teams

Our Latest Work

We strive hard to deliver result-driven digital solutions across the globe. Check out our case studies to get a glimpse of how we ideate, innovate, and create unconventional digital solutions according to the requirements of our clients.

Discover diverse and passionate insights from our tech enthusiasts. We collaborate across various sectors to streamline operations and drive innovation. Explore our rapidly growing collection of articles to see why we’re at the forefront of IT solutions.

The decision to move from Magento to Shopify is one of the most significant replatforming choices an ecommerce business can make. Magento is powerful, but its power comes with...

Accuracy gap is real: Traditional CPG forecasting carries a 25-40% MAPE error rate. AI-powered models bring that down to 8-15%, according to McKinsey research....

Real stories from global leaders who trusted us with their ideas.

Partnering with APPWRK helped us build a compliant and scalable healthcare platform, accelerating our time-to-market by 35%. Their team consistently delivered outstanding work.

Beesers

Digital Healthcare Client

Collaborating with APPWRK, Sportskeeda modernized its platform into a real-time sports engagement ecosystem, enabling seamless content delivery, scalable fan interactions, and high-velocity performance.

Sportskeeda

Sports & Entertainment Partner

Working with APPWRK was effortless. They captured our vision, maintained full compliance, and delivered a digital experience that built trust and elevated how customers interact with our fintech brand.

PayPenny

Fintech Partner

Working with APPWRK gave us confidence in adopting AI responsibly. Their team built a safe, intelligent bot that transformed how we engage with leads and helped us achieve measurable revenue growth.

IFB

AI Transformation Partner

Leveraging APPWRK’s digital expertise, Nemesis launched a scalable, compliant, and safe super app that connects content delivery, real-time communication, and logistics management within a single platform.

Nemesis

Super App Partner

Transform Credit Decisions Through Strategic AI Partnerships

Learn how collaborative AI adoption is reshaping credit scoring into a smarter, more resilient lending foundation.

AI credit scoring platform development cost starts at $18,000 (or $25–$45/hour), as the most affordable entry point compared to competitors.

U.S. lenders, banks, and fintechs are rapidly shifting from traditional credit scoring to AI-powered scoring models for faster loan approvals, lowering operating costs, and wider credit access.

Platforms use alternative data integration, fraud detection modules, and real-time credit score calculation to improve risk prediction and strengthen compliance risk assessment.

Must-have features include KYC, explainable AI, audit-ready risk platforms, continuous model retraining pipelines, and blockchain-based data validation.

Leading providers like Zest AI, Upstart, Experian, Petal, and Taktile are setting benchmarks in generative AI credit decisioning for scalable, regulator-ready solutions.

Why AI Credit Scoring Is a Tipping Point for Modern Lending?

If you’re running a bank, fintech, or lending platform, you already know the pressure is on. Margins are thinner, default rates are higher, and traditional credit decision-making rules are shutting out entire segments of borrowers. Now is the time you either adapt with AI or risk falling behind.

Here’s what’s driving the shift:

Your industry is digitising faster than ever.More than 70% of financial institutions are now investing in AI and Data Analytics. The reason is simple: you need sharper decision intelligence, less operational complexity, and systems that can handle the stakes of modern lending.

AI isn’t a theory anymore.McKinsey reports that one in five U.S. banks already use NLP and OCR to parse financial documents and speed up loan applications. Another 60% are planning to adopt deep learning models, ensemble trees, and predictive analytics within the next year. If your competitors are building this muscle, you can’t afford to wait.

Consumers are tired of being excluded. Last year, 43% of U.S. SMEloan applications were denied, mostly because traditional models fail anyone with thin or limited credit histories. With AI, you can expand access to credit by analysing social media activity, online purchases, or employment patterns. Imagine being the lender who says “yes” when others can only say “no.”

Regulators want transparency. Compliance with the Fair Credit Reporting Act and state-level lending rules is pushing every lender to prove their credit decision-making frameworks are fair and free from systemic bias. AI tools with interpretability features give you that safeguard.

The economy is unforgiving. Rising interest rates, heavier debt loads, and higher NPLs mean mistakes cost more than ever. AI-powered credit scoring systems help you keep losses under control, approve faster, and maintain resilience across the economy.

So if you’re a CTO, product head, or founder in New York, APAC, or South Africa, the real question isn’t whether AI is worth it. The question is: how quickly can you make the transition without losing customers to lenders who already have?

How AI Is Used in Credit Scoring and Credit Risk Management?

AI credit scoring platforms are changing how institutions assess risk. Instead of relying only on credit history and rigid traditional models like FICO or VantageScore, today’s systems pull from alternative data sources, apply machine learning and deep learning, and use continuous learning loops. The result is faster credit decision-making, fewer cases of exclusion, and smarter ways to evaluate creditworthiness across industries.

Leveraging Alternative Data for Credit Scoring

AI models go beyond the basics of income, employment, or prior loans. They factor in rental payments, utility bills, online purchases, and even social media activity. This shift gives lenders a clearer figure of thin-file borrowers, gig workers, and SMEs with limited credit histories. For borrowers, it means more access to credit. For lenders, it means higher approval rates without spiking default rates.

Real-Time Analysis in Credit Decisioning

With NLP, OCR, and predictive analytics, AI platforms can parse financial documents in seconds. No more waiting days for manual credit underwriting. Lenders can greenlight or decline loan applications almost instantly, cutting operational complexity and improving portfolio reliability.

Pattern Recognition for Better Risk Prediction

AI-powered systems detect signals in customer data that older risk models miss. Think subtle spending trends, unusual debt patterns, or repayment shifts. Using trees, regression, and ensemble methods, lenders spot risks early and protect their portfolios from NPL spikes. [MDPI, 2019]

Platforms from providers like Zest AI and Upstart excel in detecting subtle repayment risks through pattern recognition.

Continuous Learning for Smarter Models

Unlike static credit scoring systems, AI platforms improve daily. Each transaction, each generation of borrower data, strengthens the model. Continuous retraining pipelines adjust for interest rates, shifts in the economy, or new fraud tactics. For CTOs, this means a system that grows smarter with time instead of growing outdated.

Use Cases of AI Credit Scoring in Credit Risk

Lending Segment

Traditional Model in Credit Scoring in Lending

AI Credit Scoring Model

Personal Loans

Approvals based only on credit bureau history

AI-powered credit scoring for personal loans using alternative data + faster decisions

SME Lending

Thin-file SMEs are denied due to a lack of history

AI-based credit scoring with cash-flow underwriting & alternative data integration

AI-powered credit scoring for banks with explainable AI + compliance

Collections & Recovery

Reactive approach

Optimising collections with continuous learning

Fraud Prevention

Limited fraud checks

Fraud detection modules with real-time monitoring

AI in Credit Decision and Underwriting

AI automates the evaluation of eligibility ratios, flags missing documents, and scores loan applications at scale. These platforms function as automated engines for loan origination and underwriting, cutting manual effort and ensuring consistent creditworthiness evaluations. This frees credit officers from manual checks and raises both speed and accuracy in credit underwriting.

Client Engagement Through Generative AI

Generative AI tailors products to consumers by blending customer data, behaviour, and risk profiles. Instead of offering one-size-fits-all loans, lenders can hyper-personalise terms. The payoff: higher conversions, stronger loyalty, and reduced bias in product offerings.

Fraud Detection and Risk Identification

Fraud isn’t a once-a-quarter rule check anymore. AI continuously monitors transactions, validates identity, and flags anomalies in real time. This proactive approach keeps both the institution and the borrower safe while ensuring smoother compliance checks.

Compliance Risk Assessment for Regulatory Benchmarks

Regulators demand fairness and transparency. With interpretability features, audit trails, and compliance-ready frameworks, AI systems align with the Fair Credit Reporting Act, CFPB mandates, and the EU AI Act. This minimises stakes for lenders while ensuring every decision is defensible.

Modern platforms double as audit-ready risk systems, embedding Basel III tools and reporting frameworks aligned with global compliance standards.

Data-Driven Decision-Making for Lenders

By combining Data Analytics, NLP, and deep learning, lenders can analyse structured and unstructured data at scale. These insights improve credit decision-making, cut debt exposure, and strengthen long-term portfolio inflows.

Expanding Loan Approvals

AI models unlock credit for consumers that traditional models reject. By using alternative data sources like employment records, utility bills, and social media activity, lenders approve more loans while controlling default rates.

Examples: Upstart, LendingClub, Kabbage

SME Lending with Alternative Data

SMEs often lack formal credit histories, making financing difficult. AI-based platforms consider invoices, cash flow, and digital activity. The outcome: fairer credit decision-making that still meets regulatory rules.

Examples: Kueski, Biz2X, OnDeck

Explainable Credit Risk in Regulated Markets

In regulated markets like the U.S. (CFPB), Europe (EU AI Act), or India and South Africa, interpretability is non-negotiable. Platforms from Zest AI, Experian, and FICO demonstrate how explainable AI meets compliance while preventing borrower exclusion.

Global players such as Experian and Taktile provide explainable AI tools to help lenders align with CFPB and EU AI Act benchmarks.

Personal Lending at Scale

With AI, lenders can approve personal loans in hours instead of weeks. By automating credit underwriting and tailoring offers to consumers, lenders scale lending without sacrificing safety.

Examples: LendingClub, Petal, SoFi

Real-Time Risk Assessment for BNPL

BNPL is exploding, but so are risks. AI systems calculate credit scores in real time, spot risky repayment behaviours, and act as early-warning signals for defaults. This keeps default rates under control while supporting the transition to faster, consumer-friendly credit.

With these use cases, credit risk organisations are proving that AI can optimise underwriting, expand customer access, and meet compliance guardrails, all while lowering costs and improving risk precision.

How Much Does It Cost to Develop an AI Credit Scoring Platform?

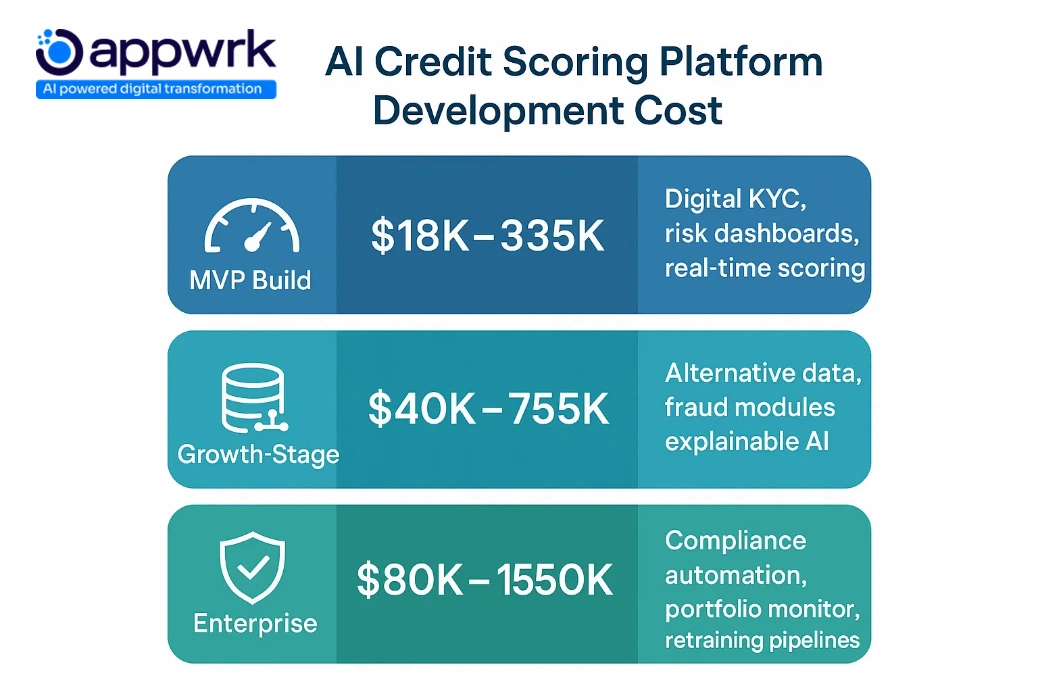

AI credit scoring platform development cost starts at $18,000 (or $25–$45/hour), with enterprise builds reaching $150,000 depending on compliance and features:

MVP Build (Lean Model): $18,000 to $35,000 Includes core features like digital KYC, risk dashboards, and real-time credit decision-making. Ideal for startups testing thin-file consumers or fintechs exploring market trends.

Growth-Stage Platform: $40,000 to $75,000 Adds alternative data sources, fraud detection, predictive analytics, and explainable AI. This tier helps lenders expand access to credit for borrowers with limited credit histories while maintaining strong risk frameworks.

Enterprise Deployment: $80,000 to $150,000 Designed for banks and large institutions. Features include full compliance automation, deep learning models, continuous retraining pipelines, and portfolio monitoring at scale.

Unlike traditional builds, modern platforms cut costs by using API-first architectures, open-source libraries, and modular frameworks. This lowers complexity, speeds rollout, and ensures lenders can adapt quickly to new regulatory rules like the Fair Credit Reporting Act.

The takeaway: costs are flexible, but with the right partner, like Appwrk, you can launch faster, safer, and cheaper than legacy vendors, without sacrificing compliance or accuracy.

What Are the Biggest Challenges of AI in Credit Scoring and How to Overcome Them?

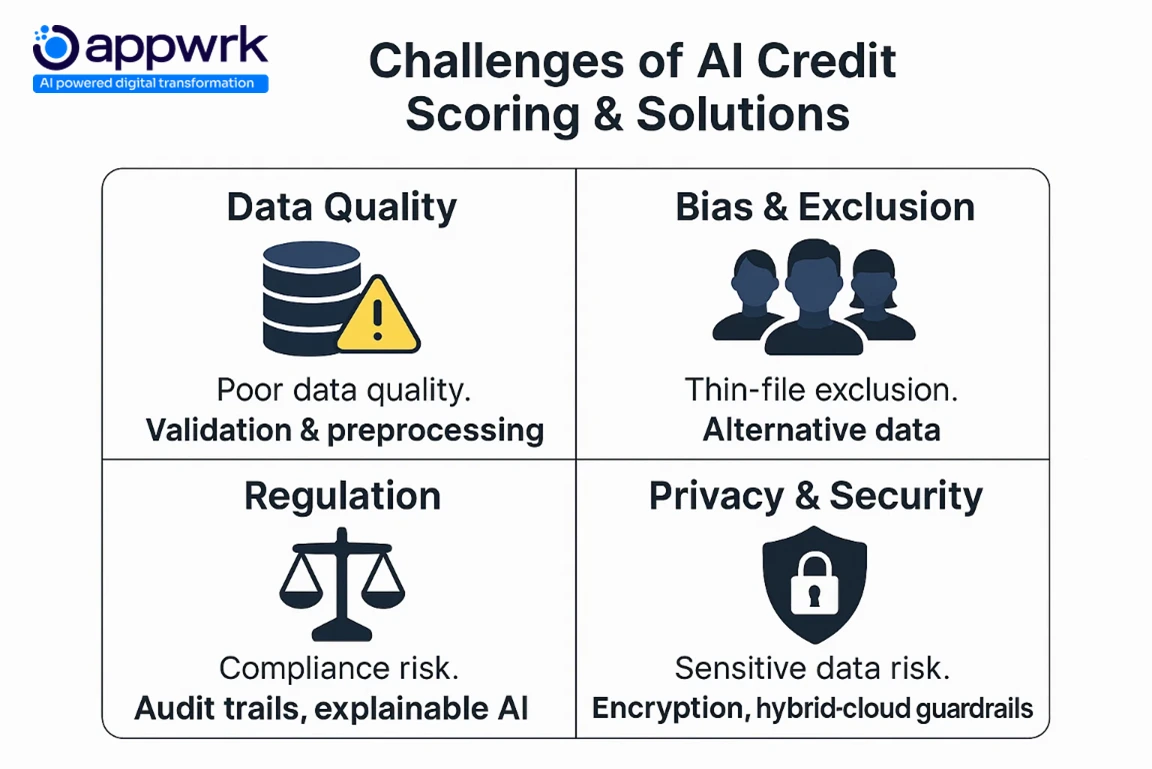

AI credit scoring is transforming how lenders evaluate creditworthiness. But without guardrails, risks like bias, unreliable data, and regulatory gaps can derail deployments. Here’s how to overcome the biggest hurdles in credit scoring:

1. Data Quality & Reliability

Challenge: Poor customer data, missing financial documents, and unstructured inputs reduce fairness and skew evaluation.

Solution: Build ingestion and preprocessing pipelines with normalization, enrichment, and OCR validation.

Outcome: Cleaner data improves scoring reliability, reduces default rates, and creates audit-ready outputs for regulators.

2. Bias & Exclusion

Challenge: Thin-file borrowers or gig workers face exclusion when models rely only on bureau histories.

Solution: Leverage alternative data sources such as rent, utilities, and social media activity to expand risk models.

Outcome: More inclusive decisions that balance fairness with repayment precision, improving financial inclusion across industries.

3. Model Risk & Interpretability

Challenge: Complex regression ensembles and deep learning models often act like black boxes, creating explainability issues.

Solution: Apply SHAP/LIME for interpretability and embed explainable AI into decision frameworks.

Outcome: Regulators, risk teams, and consumers gain transparency into approvals and rejections, increasing trust.

4. Regulatory Complexity

Challenge: Global rules like CFPB mandates, the EU AI Act, and Basel III raise compliance stakes.

Solution: Maintain audit trails, governance models, and automated compliance checks.

Outcome: Platforms remain aligned with evolving standards, ensuring consistent, fair, and compliant credit underwriting.

Challenge: Sensitive borrower data and rising debt defaults create risks of breaches and misuse.

Solution: Deploy hybrid-cloud setups with encryption, modular guardrails, and secure data frameworks.

Outcome: Protects borrower trust, secures income and employment records, and supports large-scale adoption without exposing institutions.

By addressing these challenges, lenders don’t just prevent risk; they unlock growth. Stronger data pipelines, explainable AI, and compliance-ready risk models mean faster approvals, lower defaults, and sustainable lending in volatile economies.

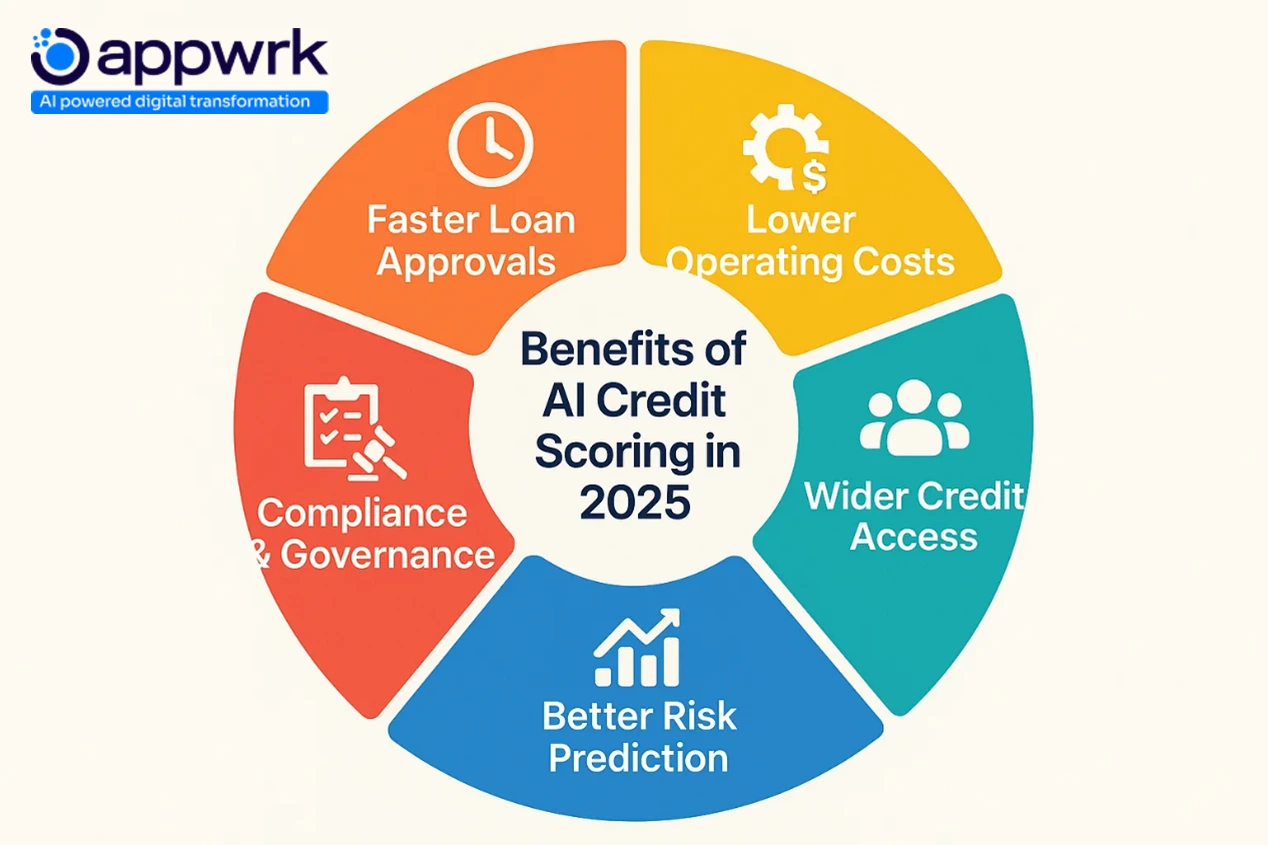

What Are the Benefits of AI Credit Scoring Across Lending Segments?

AI credit scoring is no longer just a buzzword. For institutions, from global banks to digital banks, fintech startups, and SME lenders, it’s becoming the default credit scoring system. The shift away from traditional models like FICO or VantageScore is happening fast because the gains are clear: faster loan applications, lower costs, stronger compliance, and broader access to credit for consumers with thin or limited credit histories.

Here’s how those benefits show up across the lending ecosystem:

Faster Loan Approvals With AI Credit Scoring

Think back to the days when loan applications sat in queues for manual review. AI changes that. By automating credit underwriting, parsing financial documents with OCR and NLP, and applying predictive analytics, lenders approve loans in minutes. This is crucial for gig workers in New York or South Africa, or SMEs in India that can’t wait weeks for working capital.

Lower Operating Costs Through Automation

Every manual check adds cost. AI credit scoring platforms automate evaluation workflows, cutting staff time and paperwork. MVP builds start around $18,000, a fraction of legacy systems. For CTOs, this isn’t just about saving money; it’s about freeing teams to focus on strategy instead of repetitive tasks.

Wider Credit Access Using Alternative Data

By pulling in alternative data sources like rent, utility payments, or even social media activity and online purchases, lenders can assess creditworthiness more fairly. This reduces bias, expands access to credit, and supports consumers who were invisible to legacy frameworks.

Better Risk Prediction With Machine Learning Models

AI combines deep learning, ensemble trees, and regression to analyse repayment trends and repayment signals. It predicts default rates earlier than human underwriters can, helping lenders control NPL inflows and manage debt exposures even in a volatile economy.

By integrating early-warning systems with risk mitigation tools, lenders reduce default exposure while staying fully compliant.

Tighter Compliance and Governance With Explainable AI

In regulated markets, governance is non-negotiable. AI scoring platforms include audit trails, fairness checks, and interpretability features to align with the Fair Credit Reporting Act, CFPB rules, and EU AI Act. Built-in compliance checks mean faster reporting without adding operational complexity.

Reduced Human Bias in Credit Scoring

Traditional reviews depend on human judgment, and human judgment carries bias. AI reduces that by basing credit decision-making on patterns in customer data instead of subjective rules. The outcome: higher approval rates without raising risk.

Expanded Customer Base and Financial Inclusion

For lenders, the business case is simple. By adopting AI-driven risk models, they can serve consumers with thin files, freelancers, or SMEs who have a steady income but no strong credit history. This isn’t charity, it’s opening new revenue streams across industries.

Higher Customer Satisfaction Across Lending Products

When borrowers see approvals happen quickly and transparently, trust grows. Faster processes, fairer outcomes, and fewer cases of exclusion boost loyalty for lenders, which translates into higher NPS scores and stickier relationships.

Helps in Risk Mitigation and Fraud Identification

Fraud costs money and reputation. AI platforms spot anomalies in customer data, verify employment, and track identity fraud in real time. With stronger intelligence and monitoring, lenders protect portfolios, reduce stakes, and safeguard long-term reliability.

In short, AI credit scoring isn’t just about approving more loans. It’s about reshaping the paradigm of credit: faster, fairer, more inclusive, and more aligned with the digital transition in global finance.

AI Credit Scoring vs Traditional Credit Scoring

Traditional credit scoring platforms rely heavily on structured data like payment history and income, which often exclude thin-file borrowers. AI-powered credit scoring platforms, by contrast, use machine learning models, alternative data integration, and continuous learning to deliver faster, fairer, and more accurate results.

Traditional vs AI Credit Scoring Models

Criteria

Traditional Credit Scoring

AI Credit Scoring Platform

Data Sources

Payment history, income, and credit bureau reports

Alternative data (utilities, rent, digital payments) + structured data

Speed

Days to process applications

Real-time credit score calculation

Bias

High risk of human subjectivity

Reduced human bias in credit scoring

Risk Detection

Static scorecards

Dynamic risk adjustments + pattern recognition

Compliance

Manual audits & reporting

Automated compliance risk assessment with audit trails

Scalability

Limited borrower reach

Expanded customer base & financial inclusion

Cost Efficiency

High manual overhead

Lower operating costs via automation

Why Are Enterprises Turning to AI Credit Scoring Platforms?

Enterprises aren’t just experimenting with AI credit scoring; they’re betting their future on it. Institutions know that legacy credit scoring systems built around traditional models like FICO or VantageScore can’t keep up with today’s economy, borrower trends, or compliance frameworks. The problem is simple: too much reliance on credit history, too many cases of exclusion, and too much complexity in underwriting.

AI fixes that. By combining alternative data sources with predictive analytics, deep learning, and NLP, these platforms evaluate creditworthiness in real time. They spot signals of default earlier, personalise rates for consumers with thin files or limited credit histories, and give CTOs the tools to modernise risk workflows without blowing up costs.

The payoff? Faster decisions, lower costs, and a clear path to scaling loans without raising default rates.

Lower Operating Costs

Legacy underwriting means endless documents, manual reviews, and rising staff costs. AI automates all that. Gen AI agents can parse financial documents with OCR, run credit underwriting checks, and flag gaps in customer data. For lenders, this reduces overhead and adds reliability by creating modular workflows that can reuse APIs and open-source libraries. The result: faster processing and a leaner paradigm for enterprise lending.

Faster Decisions

Borrowers don’t want to wait days for answers. Using ensemble models, trees, regression, and neural networks, AI enables instant credit decision-making. Enterprises deploy API-first systems that plug directly into LOS or digital banks. The outcome: quickerloan applications, transparent evaluation, and lower operational stakes.

Wider Credit Access

AI platforms widen the funnel by integrating social media activity, mobile usage, rent payments, and online purchases into risk assessments. For gig workers in New York or South Africa, or SMEs in India, this means real access to credit for the first time. For lenders, it means capturing untapped segments across industries while keeping debt exposure in check.

Tighter Compliance and Governance

In regulated markets, governance isn’t optional; it’s survival. AI platforms provide audit trails, fairness checks, and interpretability features that align with the Fair Credit Reporting Act, CFPB, CRA, and EU AI Act. Built-in compliance checks reduce the burden on internal teams while ensuring every rule is followed. Enterprises that once feared regulatory roadblocks now use AI to accelerate innovation while staying compliant.

Better Risk Prediction

AI is more than automation; it’s foresight. By combining Data Analytics with deep learning, platforms act as early-warning systems, spotting repayment risks long before defaults show up. They flag policy breaches, monitor NPL inflows, and predict shifts in interest rates or borrower income. With dashboards that visualise risk in real time, lenders can adjust risk models, strengthen collections, and protect long-term portfolio health.

What Are the Must-Have Features in an AI Credit Scoring Platform?

For any institution looking to scale, the question isn’t “should we adopt AI?”, it’s “how do we deploy it safely, compliantly, and profitably?” A modern AI credit scoring system has to do more than crunch numbers. It needs to absorb alternative data sources, run predictive analytics, and deliver transparent credit decision-making without creating new bias or regulatory risks.

Here are the must-have features lenders cannot afford to overlook:

User Registration and Digital KYC

Onboarding is the first compliance checkpoint. Consumers expect smooth sign-up flows, but regulators demand strict checks. Digital KYC, powered by OCR and NLP, verifies financial documents and employment records in minutes. That balance of user-friendly and regulator-ready builds trust early.

Data Ingestion and Preprocessing Pipelines

AI is only as good as its data. Clean, structured, and pre-processed customer data, from bank statements to social media activity, ensures models stay accurate. Poor pipelines create complexity, unreliable outputs, and bad credit evaluations that can raise default rates.

Real-Time Credit Score Calculation

Legacy systems needed days to processloan applications. API-first credit scoring now delivers instant scores that relationship managers and CTOs can act on immediately. Faster insights mean lower stakes when approving thin-file borrowers or new SME clients.

Alternative Data Integration

To expand access to credit, platforms must ingest non-traditional data, utility payments, phone records, and even online purchases. This helps assess creditworthiness for gig workers in New York, small business owners in India, or freelancers in South Africa who lack long credit histories.

Risk Assessment Dashboards

Executives need clarity, not code. Interactive dashboards flag repayment signals, visualise portfolio health, and surface trends that traditional models like FICO or VantageScore often miss. That foresight reduces NPL inflows and optimises recovery strategies.

Fraud Detection Modules

Real-time fraud prevention is non-negotiable. AI agents scan documents, spot anomalies in customer data, and detect fake accounts before they impact institutions. Strong fraud modules protect both consumers and lenders from rising debt risks.

Customer Support and Dispute Resolution

Disputes are expensive. LLM-powered chatbots and voice agents handle common queries, draft responses, and resolve issues faster. This keeps consumers engaged while freeing human agents for complex cases.

Security and Encryption Controls

Hybrid-cloud platforms must protect sensitive credit history and income data. End-to-end encryption plus compliance checks aligned with Fair Credit Reporting Act rules ensure no compromises between interpretability, speed, and security.

Audit Trails and Regulatory Reporting

Every decision must be defensible. Audit logs, fairness dashboards, and explainability reports let lenders prove compliance across multiple frameworks (CFPB, CRA, EU AI Act). Without them, even good decisions can fail regulatory evaluation.

Multi-Language and Localisation Support

Credit isn’t local anymore. From APAC to New York, platforms need localisation to serve diverse industries and borrower bases. Multi-language support ensures consistent governance while keeping borrowers connected.

Together, these features create a decisioning architecture that is scalable, compliant, and inclusive, exactly what today’s digital banks, fintechs, and traditional lenders need.

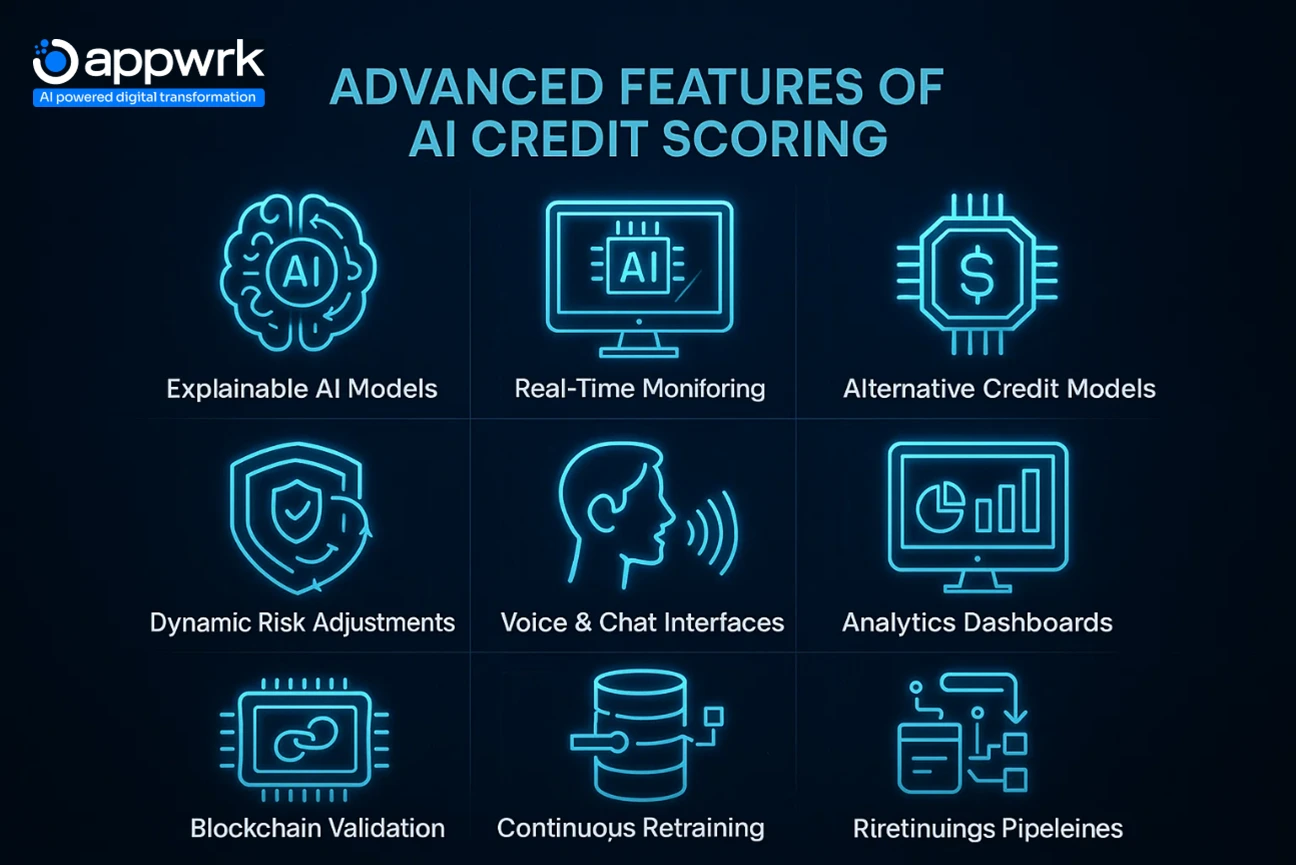

What Advanced Features Elevate an AI Credit Scoring Platform Beyond the Basics?

Basic automation isn’t enough anymore. Leading institutions are layering advanced features, deep learning, regression models, and blockchain validation on top of core systems to win trust, boost speed, and reduce bias.

Explainable AI Models

Borrowers and regulators don’t accept black boxes. Explainable AI wraps models like gradient boosting, trees, and neural nets with SHAP or LIME. This ensures outcomes are transparent, fair, and aligned with rule-based frameworks like the Fair Credit Reporting Act.

Real-Time Credit Monitoring

Continuous portfolio monitoring turns raw data into actionable signals. Early-warning systems flag repayment risks and shifting interest rates, giving lenders time to intervene before defaults damage the bottom line.

Alternative Credit Scoring Models

Go beyond bureaus. Platforms now merge credit history with alternative data sources (like social media activity) to unlock approvals without raising default rates. For example, WeBank in China and MYBank in APAC markets use this to serve new borrower segments.

Dynamic Risk Adjustments

Borrower profiles aren’t static. AI updates risk models in real time as new customer data flows in. That means smarter credit underwriting, fewer errors, and better outcomes across industries.

Voice and Chat Interfaces

LLM-driven chatbots engage borrowers naturally. They explain interest rates, handle disputes, and even walk consumers through repayment options. For lenders, that’s scalable customer care with lower costs.

Advanced Analytics Dashboards

Data Analytics and visualisation tools help lenders uncover non-linear figures in repayment behaviour. Deloittereports that dashboards with actionable predictive analytics improve collection strategies and reduce debt write-offs by up to 20%.

Blockchain-Based Data Validation

Blockchain prevents tampering. Every transaction, from loan applications to repayment schedules, is logged immutably, ensuring trust with institutions, regulators, and consumers.

Continuous Model Retraining Pipelines

Markets shift daily. Continuous retraining with fresh borrower documents and transaction flows ensures AI models evolve alongside the generation of new data. This boosts accuracy, reduces bias, and maintains compliance during digital transitions.

What’s the Roadmap to Implementing AI Credit Scoring at Scale?

Building a high-performing AI credit scoring platform isn’t just about writing code. For any institution, it’s about following a clear roadmap that balances innovation, compliance, and trust. Skip steps, and you risk biased credit evaluations, unreliable risk models, or higher default rates. Get it right, and you unlock fasterloan applications, better access for consumers, and lower long-term costs.

The roadmap looks different depending on whether you’re a large enterprise or a growth-stage fintech.

Enterprise Implementation Roadmap

Phase 1 (Months 1–6): Foundation Lay down a modular architecture with user experience, business logic, and infrastructure layers. Build data ingestion pipelines, run privacy guardrails, and ensure compliance with frameworks like the Fair Credit Reporting Act.

Phase 2 (Months 7–12): Pilot Development Test your AI credit scoring system on a limited portfolio. Use gen AI to scan financial documents, catch missing data, and share transparent results with regulators. Early predictive analytics and fairness checks reduce bias before full launch.

Phase 3 (Months 13–18): Controlled Rollout Deploy across select business units. Reuse existing APIs, measure real-world credit decision-making confidence, and compare results against traditional models like FICO and VantageScore.

Phase 4 (Months 19–24): Scaling Expand into hybrid-cloud environments, integrate with core banking and LOS, and establish a centre of excellence (CoE). This ensures repeatability and long-term reliability while adapting to new trends in regulation and technology.

Growth-Stage Implementation Roadmap

Phase 1 (Months 1–2): Rapid Assessment Identify thin-file borrowers and alternative data sources, such as rent or mobile transactions. Map risks, compile customer data, and prepare for compliance checks.

Phase 2 (Months 3–6): Implementation Adopt modular APIs for quick integration. Leverage production-ready AI libraries for faster time-to-market. Many digital banks in APAC and South Africa follow this path to reach underserved gig workers.

Phase 3 (Months 7–12): Production Deployment Go live with subsegment-specific strategies, continuous retraining pipelines, and fairness dashboards. Ensure every decision is explainable and compliant, especially as default rates, interest rates, and employment levels fluctuate with the economy.

With this roadmap, lenders move from pilots to production with confidence, avoiding costly delays and creating sustainable, transparent credit underwriting workflows.

Which Top Providers Are Leading Generative AI Credit Scoring?

The AI credit scoring market has become a battleground. Leading providers are moving past traditional models and into deep learning, NLP, and Data Analytics to set new standards for fairness, inclusion, and speed.

Zest AI

Zest AI specialises in alternative credit scoring models and explainable AI. It helps lenders assess borrowers with limited credit histories using structured and unstructured data. Its dashboards highlight signals of repayment stress early, improving approvals without spiking default rates.

Upstart

Upstart is known for using regression, trees, and neural networks to refine credit underwriting. By analysing thousands of data points, including employment, income, and online purchases, it approves moreloan applications while reducing exposure to debt.

Experian

Experian blends bureau data from TransUnion and FICO benchmarks with AI-driven risk models. Its API-first tools integrate directly with LOS and core banking platforms, making it enterprise-ready. Deloitte cites Experian as a case study in digital transformation for large-scale institutions.

Petal

Petal’s focus is inclusion. By tapping alternative data sources like social media activity and rent payments, Petal expands access to credit for excluded borrowers. Transparent, audit-ready processes make it attractive to regulators.

Taktile

Taktile offers modular credit decisioning with reusable gen AI services. Its architecture reduces complexity, accelerates deployment, and gives CTOs flexible control over their credit strategies. Many industries use Taktile to adapt to changing rules and market trends quickly.

Together, these providers show how far the market has moved from traditional models to next-gen AI platforms. Whether it’s WeBank in China, MYBank in APAC, or American Express in New York, the message is clear: the winners are those who adopt AI credit scoring systems that balance fairness, compliance, and growth.

How Does AI Credit Scoring Meet Regulatory and Compliance Requirements?

For lenders, speed is worthless without trust. Regulators in the U.S., EU, and APAC are raising the bar, and every institution must prove that its AI credit scoring system balances accuracy, fairness, and security.

The challenge? Algorithms can drift, introduce bias, or mishandle consumer data if left unchecked. That’s why compliance is about more than passing audits; it’s about building systems that regulators, auditors, and consumers alike can rely on.

Key compliance focus areas:

CFPB mandates (U.S.) → Require explainable credit decision-making that protects consumers against unfair exclusions. Every denial must be backed by auditable credit evaluations, not black-box outputs.

EU AI Act → Classifies AI scoring as “high-risk.” Platforms must provide transparency, audit trails, and structured frameworks for explainability. Non-compliance could stall enterprise-wide digital transformation.

CRA (Community Reinvestment Act) → Prevents discriminatory scoring and ensures equal access to credit across industries and demographics, including borrowers with limited credit histories.

Audit Trails & Early-Warning Systems (EWS) → Platforms must log signals, produce structured reports, and flag early default rates. This helps regulators and lenders understand why a loan was approved or denied.

Governance and Talent Models → Enterprises are forming Centres of Excellence (CoEs) with cross-disciplinary talent, compliance officers, data scientists, and credit underwriting experts, to reduce complexity, improve interpretability, and align with global rules like the Fair Credit Reporting Act.

Bottom line: compliance is not a box-tick exercise. It’s the guardrail that lets AI scale safely, avoiding debt traps and reputational damage while ensuring fair treatment of consumers.

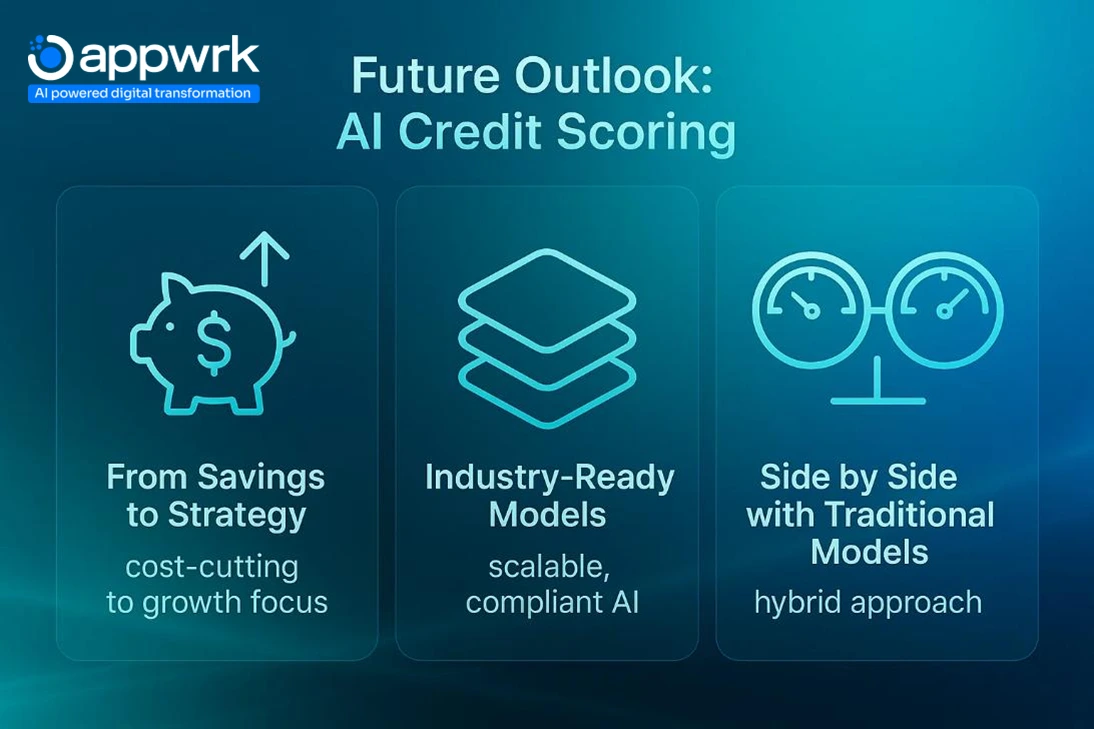

What’s the Future Outlook for AI Credit Scoring Platforms for Modern Enterprises?

The global economy is shifting, interest rates are fluctuating, and regulatory frameworks are tightening. Against this backdrop, AI credit scoring is moving from experimental pilots to enterprise-grade adoption, a paradigm shift that redefines how institutions approach risk. As adoption accelerates, lenders are increasingly relying on proven AI credit scoring providers such as Zest AI, Upstart, Experian, Petal, and Taktile as long-term infrastructure partners.

Shift From Cost Savings to Strategic Growth

AI credit scoring started with cutting costs with faster approvals, fewer documents, and shorter processing times. The future is bigger: AI will become part of core credit underwriting, helping lenders design personalized loan offers and monitor portfolios more effectively. It’s not just efficiency anymore; it’s about long-term growth.

Industry-Ready Models

Future AI platforms will use machine learning, deep learning, and natural language processing (NLP) to combine financial documents with alternative data like rent payments or social media activity. This means decisions will be faster, more transparent, and more inclusive while staying compliant with lending regulations.

Hybrid Phase With Traditional Credit Scores

AI won’t instantly replace FICO or VantageScore. Instead, lenders will use both side by side. Traditional models act as a baseline, while AI offers deeper insights and more accurate risk detection. Over time, as AI proves reliable, it will take the lead in approving more complex loan applications.

In short, the future of AI credit scoring is about moving from simple cost-cutting tools to strategic, compliance-ready platforms that expand access to credit, reduce risk, and reshape lending.

How Appwrk Can Help in AI Credit Scoring Platform Development

For banks, fintechs, and institutions, the question isn’t whether to adopt AI credit scoring; it’s how to do it without overspending or exposing themselves to bias, compliance risks, or unnecessary complexity.

At Appwrk, we build cost-effective AI credit scoring systems that scale with your business model. Whether you’re a growth-stage startup serving gig workers in India or a large enterprise bank in New York, our solutions balance innovation with regulatory guardrails.

Lean MVPs from $18,000 → Launch a Minimum Viable Product in weeks with digital KYC, real-time scoring, and API-first integrations.

Enterprise-grade builds → Add advanced modules like explainable AI, predictive analytics, and fraud signal detection that meet Fair Credit Reporting Act and EU AI Act requirements.

Seamless integrations → Our platforms connect with LOS, core banking, and third-party APIs. We’ve built systems that handle loan applications, financial documents, and alternative data sources such as social media activity and online purchases.

Scalable & secure → We use modular frameworks, encryption, and continuous retraining pipelines to ensure reliability, fairness, and compliance.

By combining ready-to-deploy modules with custom builds, Appwrk helps lenders improve creditworthiness evaluation, expand access to credit for borrowers with limited credit histories, and keep default rates in check, all while reducing operating costs.

Partner with Appwrk to launch faster, safer, and smarter. You’ll move from pilot to production without the budget overruns seen with traditional vendors, and you’ll be ready for the next generation of digital lending.

FAQs

Q1: How does AI credit scoring improve approval rates without increasing defaults? AI models combine credit history with alternative data sources like cash flow, rent, and mobile transactions. By spotting repayment patterns, they expand approvals while keeping default rates lower than traditional models such as FICO or VantageScore.

Q2: What is the cost to develop an AI credit scoring platform? AI credit scoring platform development costs start from $18,000 for an MVP and can scale up to $150,000 depending on features, integrations, and compliance needs. Advanced deep learning or NLP-driven builds increase budgets but also future-proof against rising interest rates and NPL inflows.

Q3: Can AI credit scoring platforms integrate with existing loan origination systems (LOS)? Yes. Modern platforms use API-first architecture to connect seamlessly with LOS, core banking, and even digital banks like WeBank and MYBank in APAC or South Africa.

Q4: How do lenders use alternative data for credit risk assessment? They combine customer data such as employment, cash flow, and social media activity with bureau data from TransUnion and American Express reports. This approach helps lenders serve excluded consumers and unlock new revenue streams across industries.

Q5: What role does generative AI (gen AI) play in credit decisioning? Gen AI transforms unstructured documents into structured insights. For example, it can process OCR scans of financial documents or online purchases and generate transparent outputs for credit underwriting.

Q6: How do AI-powered early-warning systems (EWS) reduce portfolio risk? By monitoring borrower behaviour daily, these systems flag repayment risks early. Dashboards highlight signals of stress, helping institutions adjust risk models before defaults escalate.

Q7: What are the compliance challenges under the CFPB and the EU AI Act? Lenders must meet strict rules for transparency, explainability, and fairness. That means every credit decision-making process must produce structured audit trails that regulators can review, no black boxes.

Q8: How long does it take to implement AI credit scoring in an enterprise bank? Enterprise deployments take 12–24 months, while fintechs can go live in 3–6 months with pre-built modules. Contact the Appwrk experts to know the actual timeline for your credit risk management System.

Q9: What advanced features make AI credit scoring software better than legacy models? Features like predictive analytics, fraud detection, blockchain validation, and interpretability tools ensure higher accuracy, better compliance, and fairer credit underwriting than traditional models.

Q10: Which top providers are leading AI-powered credit scoring? Providers like Zest AI, Upstart, Experian, Petal, and Taktile are setting the pace. Deloitte has also highlighted Chinese lenders and digital transformation projects in New York and India as benchmarks.

Gourav Khanna is the Co-founder and CEO of APPWRK, leading the company’s vision to deliver AI-first, scalable digital solutions for enterprises and high-growth startups. With over 16 years of leadership in technology, he is known for driving digital transformation strategies that connect business ambition with outcome-focused execution across healthcare, retail, logistics, and enterprise operations.

Recognized as a strategic industry voice, Gourav brings deep expertise in product strategy, AI adoption, and platform engineering. Through his insights, he helps decision-makers prioritize market traction, operational efficiency, and long-term ROI while building resilient, user-centric digital systems.

Subscribe to APPWRK Blogs, We'll Do the Rest!

Get Blogs on UI/UX, Mobile Apps, Online Marketing, and Web development technology.

Unlock worthy and priceless suggestions from the masters of mobile and web app development